China's Power Grid

Something we should understand a great deal more

I have recently been busy on more academic stuff and without giving the game away let me just say impart some helpful advice: if you are building big multi-commodity network flow models in Python switch to Julia and JuMP now. Existing packages in Python like PuLP, Pyomo and the like are great for smaller problems but you will hit asymptotic problem compile times and sooner than you think. I know there is a great open source community and the packages like PyPSA are superb but - and it is a big but - China will break whatever stock Python tooling you are building. China is big and complicated: when you hit networks with 50,000 edges and 10+ flow types you are going to have problems. Refactor your code to something that scales better and incur the new language cost upfront. There is an emerging world of excellent Julia tools including the NREL Sienna suite though its documentation needs work.

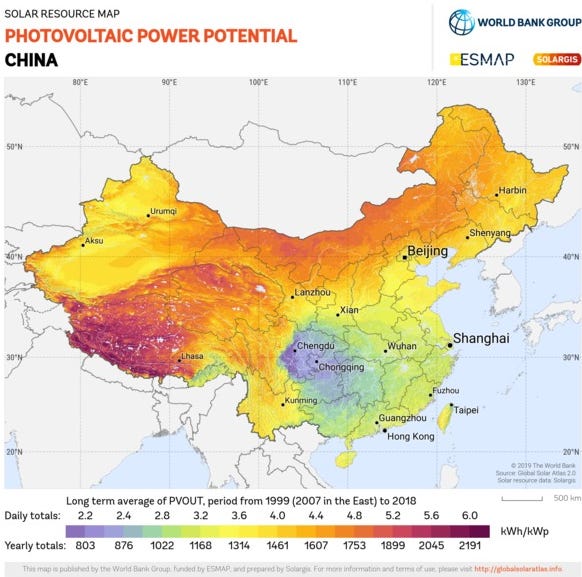

This exercise in modelling yet more coal and other things led to me to the realization that there is not really any good public modelling of China’s grid in the here and now. This is a serious gap not only in academic literature but for anyone in the business of energy trading or investing. China is still the world’s largest LNG importer and coal importer: no other country’s power grid dynamics matter more for global fuel balances. In addition, there is enough public information out there that things are happening very quickly on this grid. Firstly, China is installing solar as a staggering rate. According to Rystad China will hit a terawatt of solar capacity by 2026. Where that solar goes matters on the margin as you can see from a map of what capacity factors solar has in China but only on the margin - even at a modest 15% capacity factor this is enough to make up over 17% of China’s power demand and represents a doubling in three years. A country in the midst of a structural real estate slowdown and outright demographic decline is unlikely to have material demand growth in electrical power. This would imply that China is going to start burning less thermal coal and LNG on the margin and soon.

China is also building a similarly boggling amount of energy storage - it is hardly an option not to with this level of solar penetration. Battery storage installations are substantial in power terms but less so in energy terms (hours of storage) but China’s pumped hydro rollout is very material with respect to both with close to 200GW expected to be completed in the next five years.

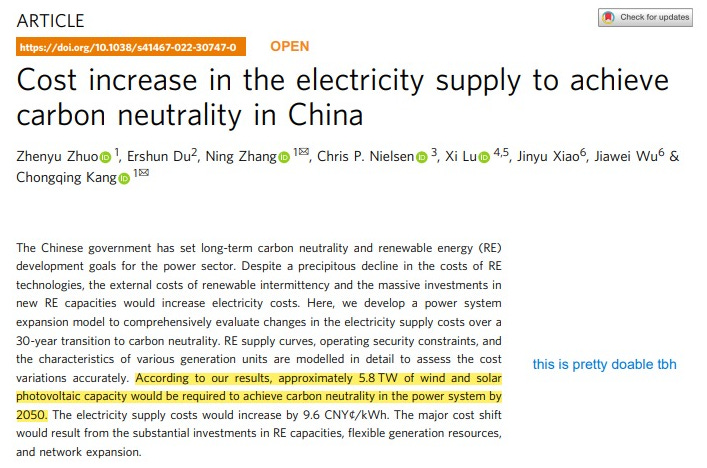

On paper all this should lead to China decarbonizing quickly. A paper modelled what it would take to completely decarbonize China by 2050 and came up with the following numbers. On current wind and solar installations China should be over 1/3 of the way there by the middle of this decade - and this paper assumes bullish power demand growth that does not tie with what we now know about the real estate sector. Peak demand of 1.9TW compared to 1.2TW today looks downright delusional. Yet even then the progress is heartening. Joseph Webster at The Atlantic Council has noted that China’s solar is going into regions close to the coast and the pumped hydro is similarly placed - this should lead to a quick displacement of both thermal coal and LNG imports for power burn.

This paper also models daily power output by source in the 2050 scenario and suggests that even using these implausibly high power demand numbers that China would need ~3TW of solar and 2TW of wind with daily output profiles as below. This all looks plausible at this point if the solar installation and production numbers are to be believed.

The problem of course is that none of these figures tie with current data. China has 490GW of solar installed as of July according to NBS and China Electricity Council data, it generated 25.9TWh in that month. That represents a capacity factor of ~7% in the middle of summer for the total but around 13-14% for utility and tracks annual variation so - the utility data is not terrible. Data for distributed solar is not included and it seems that nobody knows or if they do, it isn’t published and even academic papers in China just estimate this based upon provincial location and demand. It is also somewhat unclear how this is counted into demand which normally distributed solar would detract from. [NB this par updated after David Fishman pointed out a miscalculation].

The stakes are sharper than pontificating about what 2050 looks like or the carbon budget. For countries that are massive fossil gas and coal exporters the current rate of renewables and storage build out is enough to break global balances and soon. Tracking China’s volatile hydro output has been useful for energy traders for years but the exact size, scope and location of the renewable buildout now matters in the short run too. The growth in solar output based upon installed capacity data is now as big as the deviation in hydro output in a bad hydro year. In the medium term or a few years this could permanently break the outlook for key exports of thermal coal and LNG something which matters a very great deal to a place like Australia let alone countries with even less diverse exports and particularly those which have committed the original sin of borrowing in US dollars.

The reason grid modelling matters here is that not just the aggregates matter but where the capacity for renewables and storage goes in and how well it is connected to other parts of the country. Let me explain: if China puts 3TW of solar into Inner Mongolia and then there is no transmission capacity to use it then curtailment rates explode and the power cannot be used. In this inefficient configuration Shanghai still imports LNG and coal and China can add ghost utility PV to its ghost cities. Per the Atlantic Council piece and official data this is not what is happening, and we know from the paper that displacing LNG would only require an incremental 2.5% coal burn and that China is thinking hard about an LNG blockade. Webster is astute to think about how these changes might attenuate the Malacca Dilemma if only because China is quite clearly thinking about it too.

Instead, China is putting a lot of solar, wind and storage where the demand is. China’s LNG imports are comparatively weak and not improving - something consistent with Eastern grids that are using renewables and storage for peaking power. Things seem to be changing quickly and are consistent with a deliberate effort to reduce fuel imports in turn achieving greater self-sufficiency and decarbonization. It is remarkable that only academics seem to be focussed on this.

To that end if anyone has a good source for hourly resolution data for provincial output by generation source and demand, please get in touch. This seems a remarkably large and consequential market to leave unexamined for multiple reasons: global fuel balance, inflation, security as well as the climate.

I'm not sure the assumption of stagnant electric demand is a good one. Despite the RE bust, demand continues to grow at over 3% (through Aug) this year. Moreover, don't we have to assume the Chinese population's standard of living continues to approach Western levels? This would imply continued increases in urbanization, as well as associated increases in per capita energy usage, including electricity. We're talking more air conditioning, washing machines, dryers, misc. appliances, etc. etc.

The real conundrum with your premise is the planned growth in coal power generation in China. There is 243 GW under construction/permitted, potentially reaching 392 GW when including planned but unpermitted projects. This suggests a potential 23% to 33% increase in coal capacity from 2022 levels.

Total power gen demand CAGR's of 3% at China's scale requires an all in on every generation source type of approach. The massive solar buildout, in tandem with the increased coal gen construction, aligns more with the continued growth outlook from policy makers.

The big unknown is how the grid actuary works - of course this is not 1 grid is mode like 9 - I have looked at this in the past and know some people who have modeled it - I'll connect you