Coking Coal: Its Over

A small victory lap

Last year I wrote a paper with Professor Frank Jotzo and Dr Jorrit Gosens modelling what would happen to China’s coal imports as infrastructure was expanded both within China and with greater connectivity to Mongolia. One of the key conclusions was as Mongolia’s transport connectivity to China improved that Mongolian coking coal imports would quickly displace imports from the seaborne market and likely lead to much lower prices.

This was a bold prediction at the time. China had more or less entirely shut its border with Mongolia over COVID controls and the Russia shock was well under way leading to major dislocations across commodities. Coking coal was trading around six hundred dollars per tonne in seaborne markets and higher in China and it was wholly unclear whether there would be dry bulk shippers to move Russian product. If Russian and Mongolian coal stayed out there was no clear limit to how severely the market squeeze. Twitter’s #coaltwitter had a good laugh at the paper. We modelled what would happen if Russia and Mongolia exited and the results indicated that the model did not solve for given Chinese steel demand implying that whatever price you could nominate for a given demand there was not adequate supply.

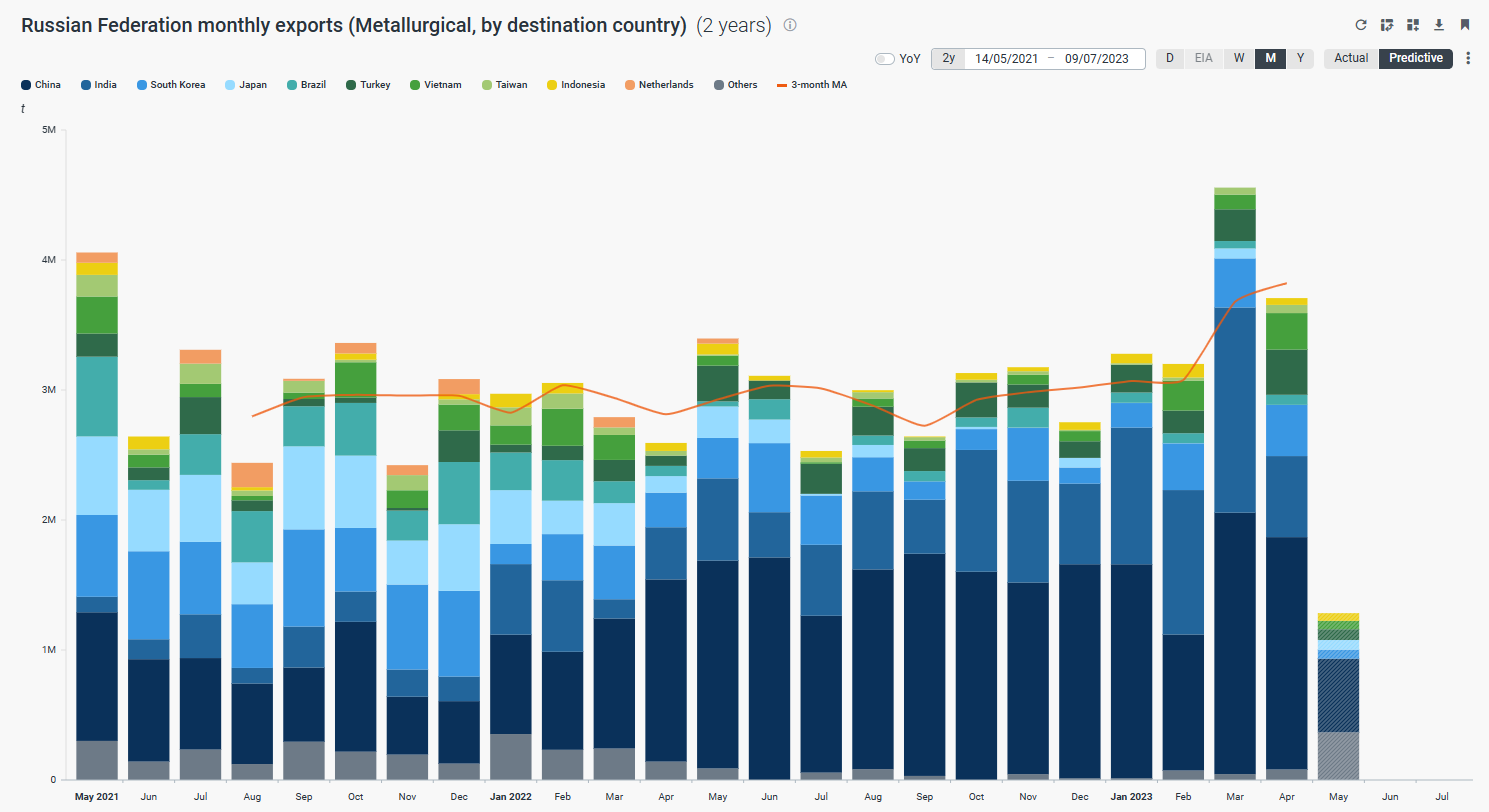

Times have changed since. Firstly, Russian exports were never interrupted and instead readily found their way to willing buyers in China, India and South Korea.

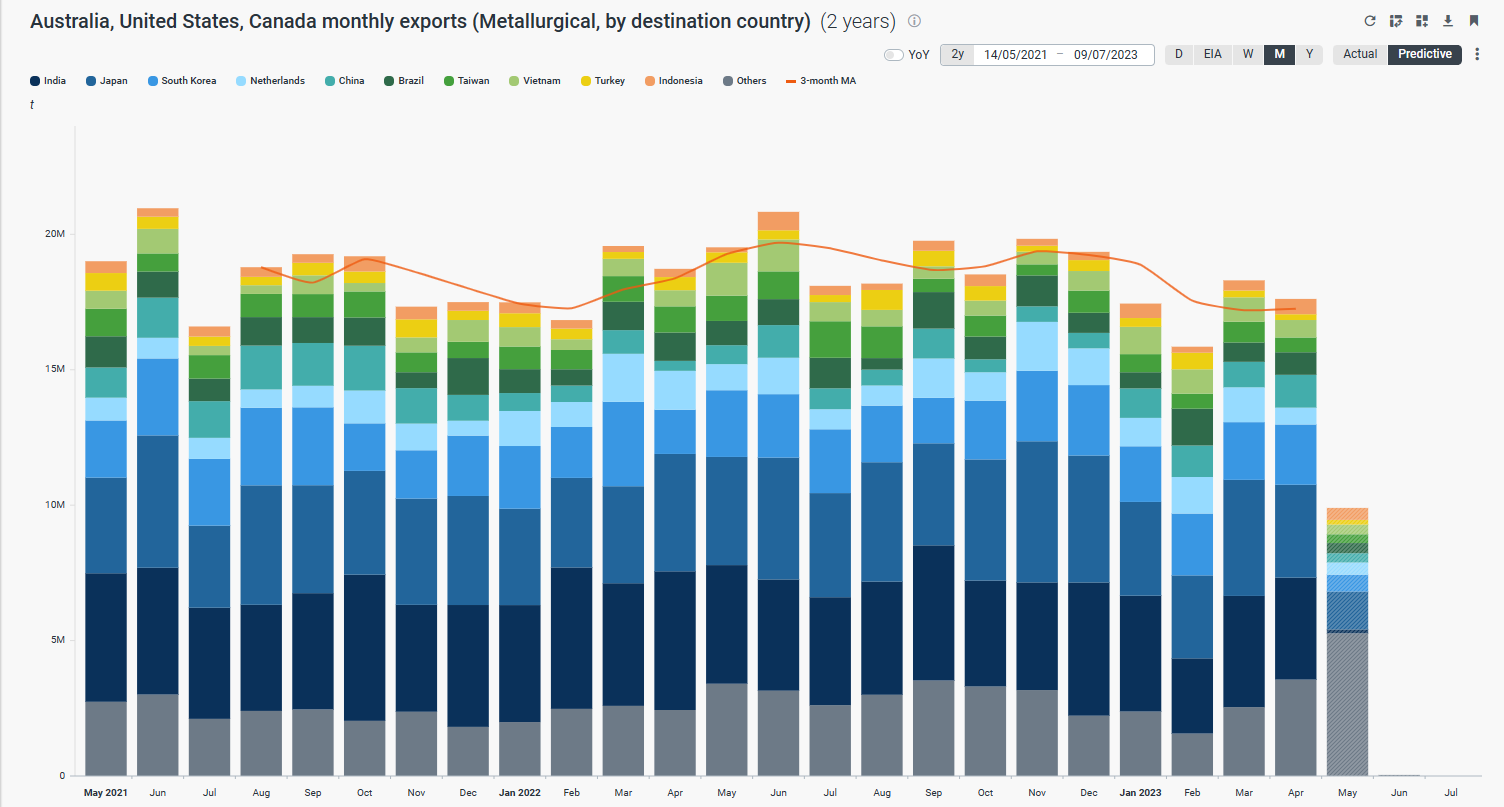

Australian, Canadian and US producers somehow could not manage a volume response to record high prices, which should lead to some questions as to how management teams of these businesses are paid: if they got lucky on a price shock but could not capitalize on it operationally then are they really worth paying bonuses to?

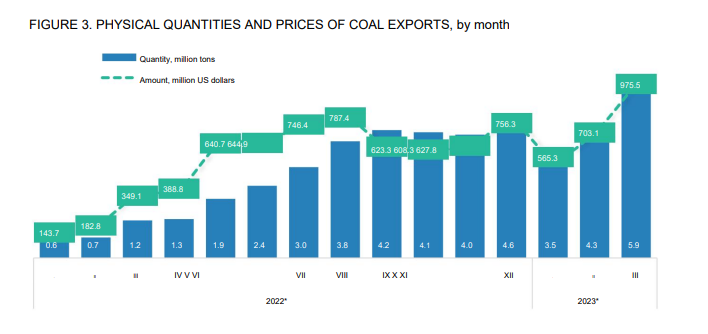

Secondly, following China’s about face in COVID related policy Mongolian exports have exploded. Commodity data services that focus on seaborne freight like Kpler do not report this but the volume uptick is very substantial. Data from Mongolian statistics is below.

Chinese imports by rail from Russia are also substantial but… they are harder to verify as both countries have been more reticent to report their trade data. There are regular news articles in Chinese state media but getting the data is challenging.

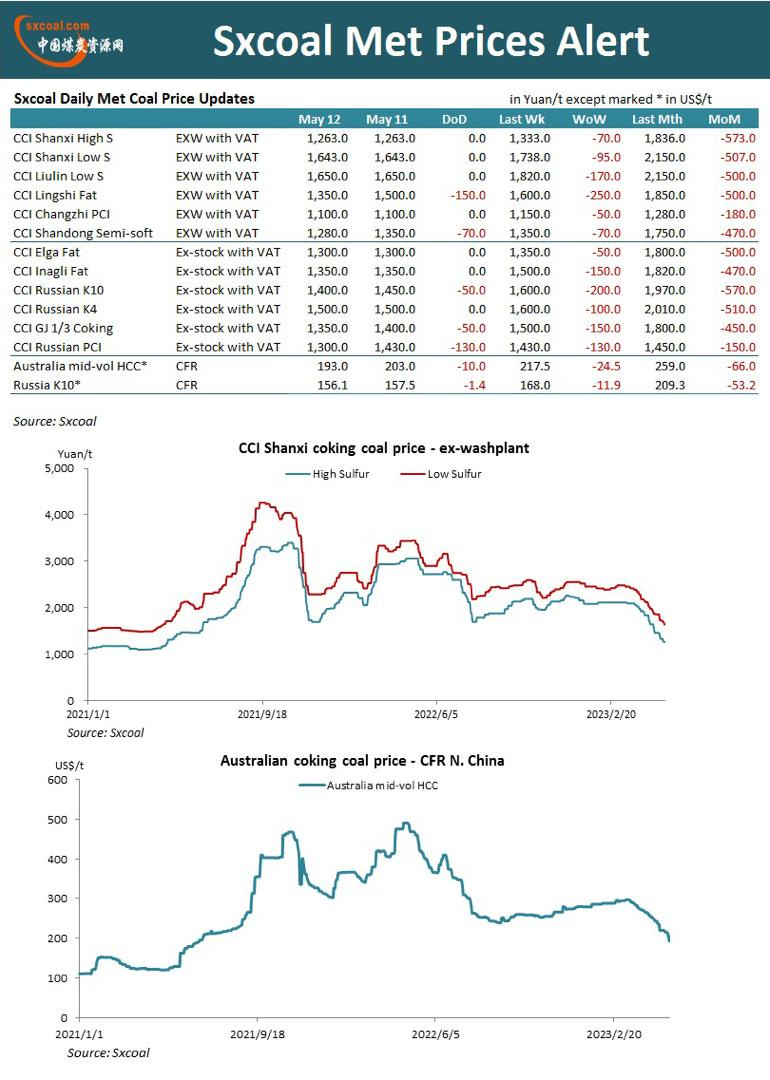

China is at the nexus of this supply expansion, so how are prices for imported coal tracking? A lot lower.

Australian import prices in particular are getting hit hard. What is notable is how poorly coking coal has performed versus other materials since China’s reopening. While many materials bounced on hopes of a China reopening and a return to investment led growth it is coking coal that has performed the worst because unlike other metals it is undergoing a substantial - yet underappreciated - positive supply shock.

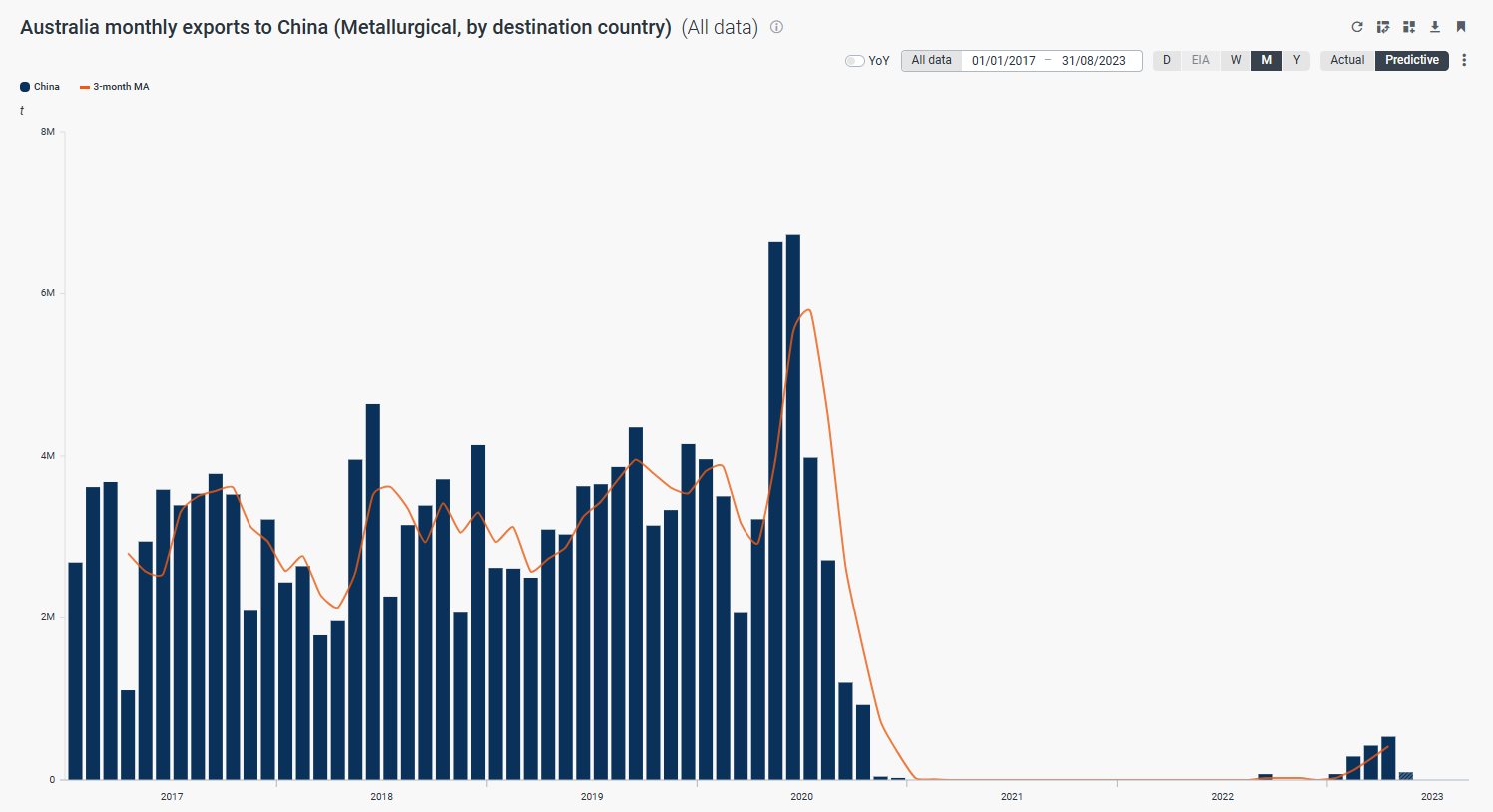

With all that it would seem to be a bad time to be approving or starting new mines and yet the bullwhip effect in commodities remains alive and well. Companies like Alpha Metallurgical are expanding output, others are raising guidance and just this week the Australian government approved a new coking coal mine at what appears to be precisely the worst time to do so. This process is far from over: Mongolian rail projects I have previously written about are nearing completion and existing rail expansions are already allowing greater flow from Mongolia at lower cost. Barring a radical return to investment and real estate led growth it is not clear what can drive a recovery in the coking coal market from here. It is no great surprise to me that China’s metallurgical coal imports upon resumption of trade with Australia have been meagre.

For investors in this space substantial stock buybacks have buttressed companies’ equities despite a slide in prices. Buybacks come to an end and coal contracts roll off leaving businesses with costs, maintenance capex and, for the foolish few, expansion capital expenditures into much weaker markets. Mongolian producers with cash costs going to $60 or less per tonne are likely to get by albeit at lower margins. US producers with all-in sustaining costs close to current spot (~$110 cash cost, $15-20 maintenance capex) are likely to get into trouble again.

But What About Thermal?

Thermal coal has two things going for it right now. Firstly, residual tightness in gas markets due to Europe’s loss of Russian gas supply which I and other have written about extensively. So long as burning coal remains cheaper than gas, it has some support from coal gas switching. This will abate over the next twelve months as US gas export supply increases but for now it helps.

Less well known and appreciate is that China’s horrific heat wave and drought in 2022 has left China with materially lower hydro power reserves going into what is forecast to be a very hot summer. While China has been gradually restricting access to power and hydro data the level of the three gorges dam says it all. China will have to backfill that missing hydro with coal imports for its Southern Grid and the surge in Indonesian imports suggest this is happening.

A heavy rainy season combined with US LNG could crash this market in due course - but for now it seems major thermal producers will not suffer as much as metallurgical coal producers. Longer term forecasting of climate and its impacts on China’s hydrology should be a focus for any coal company though I suspect they will not do that because they could not bother to cover Mongolian rail or metallurgical exports which is far easier to do.

In summary: it is back to the bad place albeit at different speeds in coal. Most producers have used the various shocks from 2021-2023 to reduce debt or diversify out of coal. Those who have chosen to double down and increase output are in for some very lean times and equity issuance as debt markets remain almost completely closed to coal producers.

Great analysis

🤣🤣🤣🤣🤣