Debunking Energy Disinformation

Election Season in Australia

It is election season in Australia which can only mean one thing: fossil lobbyist disinformation will be disseminated to journalists and if they are lazy, they will publish it without much thought or fact checking. These campaigns tend to be coordinated and have key messages so I will occasionally post the rebuttals here as the Australian election campaign proceeds.

“Renewables are Making Wholesale Energy Prices Go Up”

This is standard fare at the Australian and the like and is readily rebutted by the Australian Energy Market Operator’s Q4 system dynamics report. As you can see below, prices are only high at certain times of the day - namely around peaks when solar is not available:

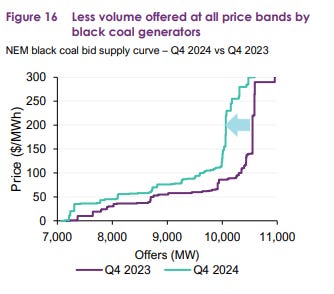

Much of these seems attributable to withdrawn black coal supply:

Which in turn has pushed up realized prices for black coal when it is the marginal MWh in the market. This is a great outcome for black coal plant owners, not so great for consumers and most definitely not the fault of renewables.

A more oblique argument might be that renewables destroy midday profitability through excess supply forcing capacity cutbacks of inflexible coal. Maybe, though that should change quickly with the rapid deployment of batteries and come at the expense of very expensive gas that sets the evening peak pricing. As can be seen below batteries are already pushing the marginal pricing power of gas out and hydro remains dominant. Given the practice of coordinated portfolio bidding by the likes of Snowy Hydro and others that own both hydro and gas assets this is as much a market competition and concentration problem as much as anything else especially since such practices have been found to be legal.

More storage owned by parties that do not own extensive fossil portfolios is the answer here and that is what is coming according to Modo Energy and BNEF. The entry of capacity outside of gentailers should be a good thing for competition in peaking hours price formation.

So why aren’t prices going down yet? A few reasons:

These batteries are not all installed yet.

Global fossil prices are still high following the Ukraine War. While LNG supply is expanding towards year end Australians eat market rate coal and gas now - legacy cost plus coal contracts are a thing of the past now in the NEM.

So long as 1 and 2 are true, fossil is high and sets the marginal MWh especially at peaking times.

Tediously for the ALP this should all change over the next 12 months but not in time for the election. One indicator of where this is going is in South Australia where wholesale price components of bills have already begun to fall despite a war and a lack of batteries. That is likely the outlook for most of Australia through 2028.

For grid investment the issue is really one of competition between distributed energy resources owned by consumers versus a regulatory framework which assumes grid services can only be provided by grid owners. Grid owners want more capital expenditures to grow their regulatory asset base to make money. Smart grid technologies and distributed technologies like renewables with storage and vehicle to grid bidirectional charging can obviate a lot of that capital expenditure. How this plays out is less a matter of what is technically possible and more who lobbies more successfully and is well covered by IEFFA here. There are some compelling signs of less regulatory capture going forward from the AEMC but this fight is far from over.

Really interesting article as usual!

Thank you for writing. This topic is confusing. https://podcasts.apple.com/de/podcast/odd-lots/id1056200096?l=en&i=1000683289906 at the end of this odd lots, Lon Huber, senior vice president of pricing and customer solutions at Duke Energy tells Tracy something like please no more solar! (She just installed some panels at her home)