European Gas and Russia

Scenarios and responses

The path of inflation and the global economy is now very much tied to the intricacies of the European energy market. I have been spending six months on this and the literature and wanted to outline what I have found and what has been thrown up as potential questions and scenarios.

Firstly, the general shape of the problem is covered well in this Bruegel piece. The image below is key:

Eastern Europe is substantially dependent upon Russian gas including Germany and while there might theoretically be headroom for Europe as a whole there are problems with:

Distributing this gas from terminals to Eastern Europe due to geographical constrainted. Possible, how much, what cost?

Questions as to whether liquefaction and LNG capacity exists to displace this and how an additional 1000TWh in a 5000TWh LNG market can be absorbed.

Second round effects on price and other countries.

Legal issues with long term LNG contracts: This is fascinating but when push comes to shove, things get done - especially if members of the EEA are exporting a lot to China which is at a bare minimum neglecting their ability to influence Putin. This would be an interesting point of leverage and I do wonder what sort of conversations are happening between the EU and Norway. China does appear to be helping a little here, but is it enough?

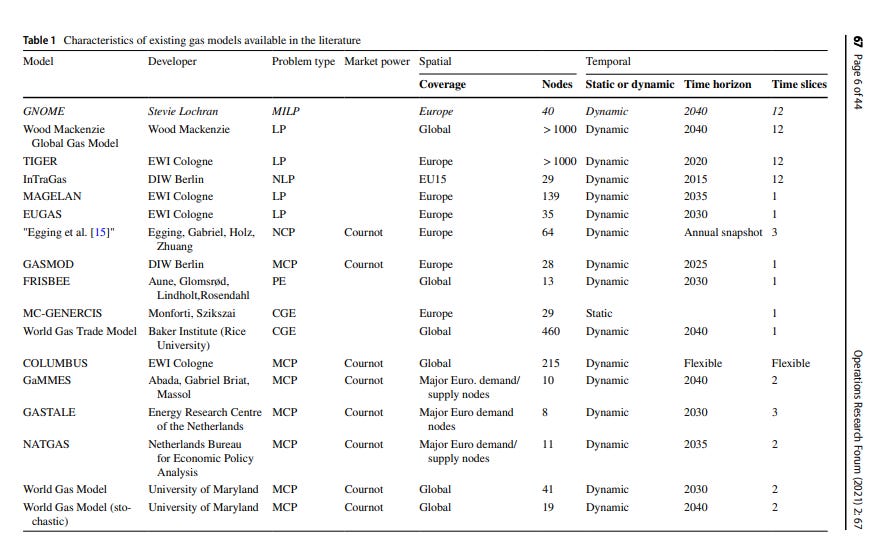

For the first question there is a whole literature of network flow optimization study and projections and it is very good and has largely been underappreciated. This paper by Stevie Lochan is excellent: firstly it is an open source model of the European gas market for multiperiod analysis way out with integrated investment decisions, secondly it is open source. Sadly, it is written in GAMS which is a proprietary operations research language. The state of play of modelling European gas markets is below, the two best products aside from Lochan’s GNOME model are proprietary and maintained by Wood Mackenzie and Cologne University:

As a very prescient fellow he ran some useful scenarios of what overall cost to Europe would be without North Stream 2:

As you can see, not substantially different before 2030 after which decarbonization should be crushing gas demand. So Nord Stream 2 was always negative NPV, which should have been a good flag to Germany’s foreign policy establishment that something else was afoot of a non-commercial nature.

Running some more scenarios on these granular models would be very timely right about now and in particular if the model results are “unfeasible” because gas cannot be supplied. In that case optimal sizing and location of LNG landing sites should be determined and broken ground on ASAP in the event Russia does cut supplies.

A related paper is also worth a look and quite clearly academics were well aware of these hard tradeoffs between Russia reliance and being exposed to global commodity prices.

In fact with Russia proposing the Power of Siberia 2 pipeline which would link even more gas flows to China, there is no trade off: China’s Russian imports will compete with LNG imports and gas will be a completely globalized market. It is highly unlikely Russian gas will be much cheaper than LNG going forward and will come with a nasty risk of being cut off.

In summary: we have the tools to estimate the constraints and start working out what the shortfalls are. There is very limited risk that investments previously held up for reasons unintelligible to those not in German politics will be white elephants given the Russian gas price advantage is going away and the volatility costs have gotten much worse.

So for the second and third question: until more pipelines are complete out of Russia you will have an egregious oversupply within Russia with nowhere to go until Russia builds more LNG capacity or completes pipelines to China. Outside Russia, prices will be high.

So run the model with Russia out and see what the shortfalls are - and by all accounts they are not small in the short term but are seasonal. Things will get better this summer and worse in the winter. Lauri has a good thread here:

The key questions I have and would appreciate any thoughts on are:

Are turning Germany’s nuclear plants back on an option for a few years? I understand the politics of this are hard, but so are crazy power bills.

How quickly can heating demand be switched to ground source or air based heat pumps? The pain point here is largely in Eastern Europe which has strongly seasonal gas demand for winter heating. Should there be some kind of Marshall Plan for Dandelion Energy or other providers of ground source heat pumps? If everyone spends their summer drilling ground based heat loops and rolling that out in Poland, how quickly can you crush heating and cooling demand?

How quickly can wind be installed in Eastern Europe? Here is a link to a random spot in Poland from the Global Wind Atlas . The advantage of wind is that the output is reliably strong in winter when heating demand is highest. This should quite clearly be a priority for those states that can’t get enough gas in via LNG in the short term and need to suppress or displace demand quickly.

How quickly can Europe roll out more solar? This may sound superfluous but every molecule not burned in summer can be banked for winter subject to storage constraints. Solar appears to be hitting acute oversupply again, this would seem to be a good time to go very hard on it and best of all it is quick to roll out.

Long duration storage technologies are improving quickly but do not seem ready for prime time. Are there any easy or quick expansions to pumped hydro or other storage in Europe? Even reducing gas use for diurnal cycling with batteries can be a powerful force for suppressing demand.

Floating storage and regasification units can be rolled out quickly, but how quickly? Oxford Energy’s estimates show very compelling costs and that they can be built quickly.

The cost of a new FSRU can typically represent only 50-60% of an onshore terminal and be delivered in half the time. New builds typically cost $240-300m and can be constructed in 27-36 months. FSRUs based on LNG tanker conversions cost less at £80-100m and the modifications typically take 18 months due to the long delivery times of the equipment not the shipyard conversion.

Europe would require quite a few of these and ideally have them placed in Slovenia or Northern Greece with improved gas interconnect to Hungary, Romania and the like. Estimates of how quickly these could be built would be very useful right around… now.