Factions and Finance of the GOP

Paradoxes of the America First Paradigm

To say that there is a lot going on right now would be a major understatement - especially so if you take both a professional and academic interest in the material world. Between Elon’s red guards and various pronouncements and reversals by the Trump administration it is very challenging to know what to focus on. Journalist friends have now started to “lie flat”: letting pronouncements and policy changes rot in the sun for a few days before doing any detailed analysis lest they get unwound like changes to who runs the US nuclear weapons stockpile.

There are some clear cleavages and divergences of interest within the GOP’s broad church. To name a few that I am watching:

Directorate S types versus the Hawks and American Petroleum Institute

If Russian gas returns to the market both via LNG and pipelines - and it is hard to see why Putin would support a deal that does not allow this - then that is a supply shock close to half the size of the entire global LNG market today of around 200 billion cubic meters. It is very hard to see how that squares with the interest of LNG exporters in the US gulf coast. It is very hard to see how US LNG competes with Russian gas in Europe given the Russian gas does not have liquefaction and regasification costs. It is very hard to see how the US walks from Ukraine and gets to tell Europe which gas it can buy. Something has to give here as it pits America First and Russian Friendly foreign policy against the American Petrostate. European gas demand is falling and will continue to do so - especially so if Germany were to restart any nuclear units.

I suspect this is going to be cause of serious rifts within the GOP coalition. To date Elon et al have moved faster and broke things faster than the Senate GOP can respond but that is unlikely to stay the case indefinitely unless the US has a multiyear cultural revolution.

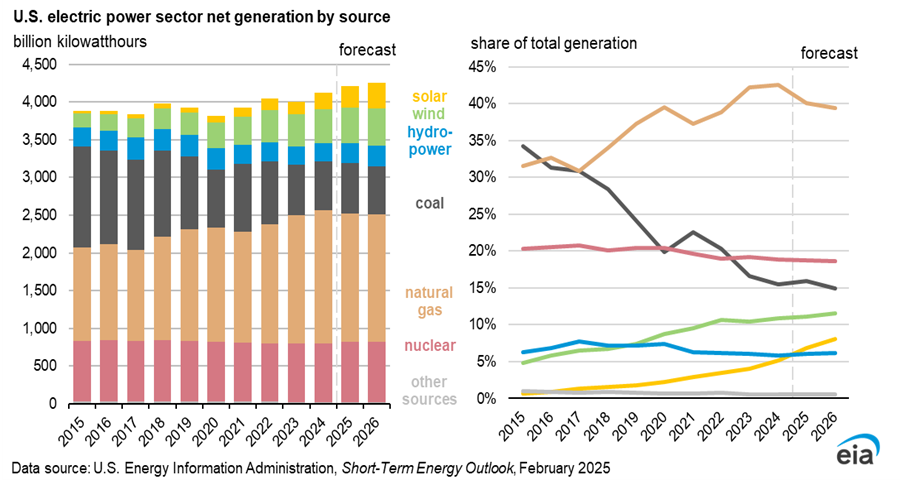

Tech Power Demand vs Owning the Libs by Blocking Renewables

As you have read elsewhere AI uses a lot of energy and AI growth in power demand at the same time as electrification of transport fleets, industry and a generally healthy US economy means power demand is going up. Read more here on datacenters and their infrastructure requirements, and here for US power demand. Most of that growth has been provided by renewables:

Short term forecasts are largely “in the bag” due to projects being constructed but how the US intends to grow power output without renewables is far from clear. GE Vernova and other providers of gas turbines are sold out through 2028 or later at this point and nuclear restarts are going to require significant help from the Loan Programs Office which the current administration appears to be shutting down as quickly as it can. Advanced geothermal is great but nascent and not particularly quick to build especially since organic Rankine plants to use the heat from below have many commonalities with conventional thermal plants. At some point “owning the libs” is going to have to come at the cost of AI dominance or load shedding - a distinctly South African experience which really rhymes with the times.

The only other option is to achieve some radical leaps in chip performance that reduce power demand. I am an investor in this space and a director of Opticore and fundamentally very bullish on these prospects - not least of all because I am fairly sceptical of endless partisan bickering delivering coherent long term-oriented policy. There are others but whether this will all arrive in time before parts of Virginia experience Johannesburg levels of power reliability remains to be seen.

Military Industrial Complex vs Military Industrial Complex

One of the more lucrative trades post-election has been shorting US defence primes and buying European ones. The story is simple enough: US wants to cut spending and pursue isolationism and Europe is going to have to step in, and that is before you consider the possibility (certainty?) that newer defence companies owned by GOP silicon valley donors are probably going to take share. This may be great for the venture capitalists but it is likely to be quite ugly for US defence industrials who are generally very good at spreading their production to marginal districts. There is a rift brewing here between how much more an isolationist US can sell into North Asia or India versus what it loses in Europe and how much it gets chipped away by Anduril and the like. This money flow into key districts has not been messed with since defence consolidation in the 1990s and well…. it may be very contentious between the GOP old school and new school.

There no doubt is more, but these rifts leave plenty of scope for division and destabilization.