Oil Demand: How Quickly Can an Ice Cube Melt?

Empirical data on the transition

Earnings season is mostly over and aside from the excitement around the thrills and spills of tech one standout sector has been energy. Oil and gas price are up, supply is not rising that quickly (yet) and inventories are tight - what a remarkable turnaround and setup from the moment Salesforce replaced Exxon in the Dow. In more volatile commodity based businesses the long run looms large but the short run drives earnings today and there is clearly a tug of war between ESG investing, longer term concerns about demand peaking for oil and the plentiful free cash flow of today. Partly this is complicated by the fact that while it is obvious that everyone driving and EV will drive oil demand much lower there is not a lot of empirical evidence to date, just anecdata from friends with EVs and solar panels in California or Sydney.

Norway has had some of the most generous and thoughtful policy on EVs for well over a decade and is a good place to look for evidence of how quickly the energy transition can move. At a high level, it seems that not much has happened as yet. Most of the decline can be attributed to people moving from diesel for heating and lighting with modest declines in road fuels. So far this does not look like the end of the world for liquids demand.

This is largely attributable to Norway’s population growth - using vehicle registration data there is a clear downtrend in the monthly consumption data per vehicle that predates COVID and lockdowns.

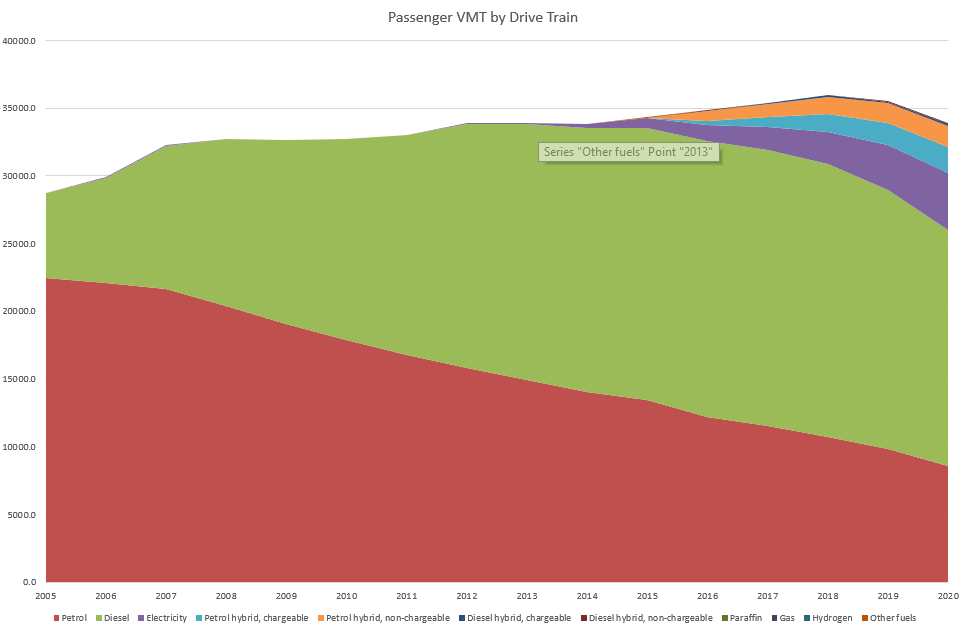

This lines up well with the change in vehicle miles traveled by drive train data:

Even though there has been consistent growth in vehicle miles traveled:

What is most notable is that like a lot of technology adoption curves the rate of change is accelerating with EV / PHEV / hybrid share growing close to 5% per annum now - Bill Gates said it better than I:

We always overestimate the change that will occur in the next two years and underestimate the change that will occur in the next ten. Don't let yourself be lulled into inaction.

There are a few important caveats here - this is passenger vehicles which are a lot of fuel demand, but not all. Heavy trucking, marine diesel (especially marine diesel) in Norway are also very big. But the contours of an accelerating pace of change are becoming quite clear. Trucking uses the same drive trains (EV and hydrogen) so when it happens it will be very fast.

For oil companies, isn’t this certain death? A slow peaking in demand followed by a rate of decline that might be faster than large scale offshore fields? Not necessarily. Reduced revenue opportunities can be offset by moving into other related areas (Exxon’s materials and resins portfolio is first class) as well as simply returning cash to shareholders and cutting capital expenditures. The path of oil, and oil stocks depends on what these companies do. If they continue to moderate spending especially in long lived projects where they might find themselves producing into demand decline and focus on shale and other short life cycle assets then they can likely do very well. Prices can be buttressed by capital discipline, capital returns will be good and shareholders will be happy even if the business overall shrinks if they get enough cash to deploy into solar, wind or other energy sources.

What would be irredeemably bearish would be a return to investing in long life assets that require strong views on prices years and years into the future. Offshore fields require years of development followed by more than a decade of production. If the new capital discipline in energy is for real then rig rates stay low and offshore services remain depressed. Any sign of that changing would be a sign that fossil energy management remains largely unchanged, and deeply problematic for investors even before you consider ESG.

Could we be in a goldilocks period of energy companies earning their cost of capital and prices being consistently above costs? Time will tell. But for this narrative to stay intact capital plans need to reflect the reality of low population growth, electrification and a flattening in liquids demand followed by outright decline - a decline that can only be “managed” with a shale heavy portfolio.

Edit 9/2: Reference tables below:

Diesel and Gasoline for cars https://www.ssb.no/en/statbank/sq/10062371

Total Vehicles: https://www.ssb.no/en/statbank/sq/10063031

Transport passenger km and tonnes-km for goods transport https://www.ssb.no/en/transport-og-reiseliv/landtransport/statistikk/innenlandsk-transport

Average light truck distance https://www.ssb.no/en/transport-og-reiseliv/landtransport/statistikk/transport-med-varebiler

China produced 3.54 million NEVs in 2021, up 181% from 2020, and more than the total of the previous three years. That's 15.7 % of the country’s entire car market.

Experts predict NEV sales of 5 - 6 million this year, 25%–30% of the domestic auto market, meaning that early education of the market is complete and the supply chain is stabilizing.