The Woeful State of US Policy on Inflation Compared to China

If you have had to spend money recently you may notice that stuff costs more. If you haven’t, good for you. But if you have you may wonder what governments can do about this. Sure if you own your own house you could get solar, a heat pump and an EV and a bumper sticker like this. But if you cannot do all those things and even if you can, you might be wondering what governments around the world are doing about this sorry state of affairs.

In the US the Fed is moving towards a level of rate hikes that would imply a recession or at least a savage slowdown in turnover of housing, autos and anything else that might require consumer borrowing. In terms of measures to reduce energy demand or facilitate substitution not much is happening. the DPA has belatedly being invoked to make heat pumps, it seems nobody had a plan for solving shortages in refining capacity despite having a lot of plans for how to help Ukraine respond to the invasion and there is some objectively unhelpful stuff being done around cutting gas taxes. Despite the ground work for sanctioning Russia and gaming out a Ukraine invasion had been done months and months prior the Pentagon clearly was not speaking to Energy or Commerce who could have done a few things well in advance:

Evaluate likely oil and products shortages: to the best of my knowledge nobody has done a graph model working out what shortages emerge if different countries are sanctioned or certain routes become unsafe or uninsurable. This is a joke and may force me to write another paper. In the meantime - people are wondering whether $3bn is took much to keep a refinery open during an oil shock? I am finding it very hard to understand very serious people these days.

$3 billion seems like a small price for the U.S. govt to pay up front (or guarantee, whatever) to get that kind of capacity back online in exchange for a cut of the upsideValero's CEO said earlier this year that it would cost $3 billion to get Lyondell's 263,776 barrel per day Houston refinery- set to be idled next year after failing to find a buyer- to get the plant to "Valero standard". This was a direct reason Valero did not purchase the plant. https://t.co/09OW35sCrD

$3 billion seems like a small price for the U.S. govt to pay up front (or guarantee, whatever) to get that kind of capacity back online in exchange for a cut of the upsideValero's CEO said earlier this year that it would cost $3 billion to get Lyondell's 263,776 barrel per day Houston refinery- set to be idled next year after failing to find a buyer- to get the plant to "Valero standard". This was a direct reason Valero did not purchase the plant. https://t.co/09OW35sCrD Laura Sanicola @LauraSanicola

Laura Sanicola @LauraSanicolaWork out response time of shale and how to speed up drilling as the risk emerged - rather than dumping SPR supplies in November. Employ America has a great piece on this and to the best of my knowledge nothing has happened yet. Doubling SPR release and buying the back end of the WTI and Brent curve til it trades flat would be a hell of a flex and likely work well. Heck, the Fed could spend less time on rates and more time on having a target for 3-18 month crude carry.

Looked at ways to speed up alternative LNG sources and landing capacity for Europe: mobile regasification platforms (FSRUs) could be secured as an option for a lot less than the cost of current inflation. These things cost about half a billion dollars - that insurance seems shockingly good value until we are much further along the path of decarbonization.

So we now find ourselves with a choice of recession or “unanchoring expectations” and other things that are very bad to monetary theorists. I do wonder about this stuff: how much of the end of 1970s inflation was Volcker and how much was the end of the Iran oil embargo, the start of the Texas oil boom and all Jimmy Carter’s demand side measures starting to bite? I’ll leave this fight to others but I think finance people give too much credit to central bankers and not enough to the starting position of countries facing a shock with regards to their power grids and transport fleet. And on these things the US has done very little and continues to do very little despite having a large domestic energy sector with short cycles from drilling to production. This is absolutely not a “recession we had to have”.

Meanwhile in China

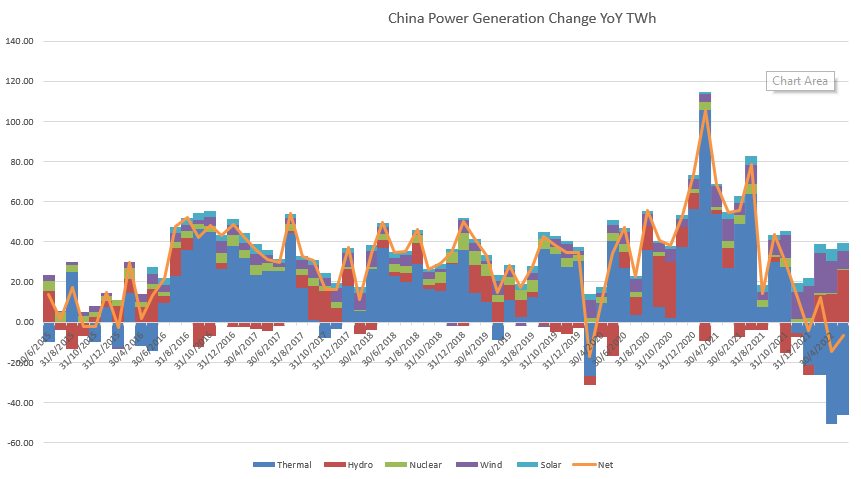

I wrote a piece last year on how a combination of an anti-corruption campaign, a hot summer, low hydro output and a red hot economy led to rolling blackouts and power cuts in Guangdong. China learned from that mess and onshore coal futures retreated quickly as mine output was increased quickly in advance of winter. China is now sitting on record coal inventories and hydro power output is very strong this year with coal and power prices largely regulated into an orderly range.

The climate implications of leaning harder into coal are dire but China is also expanding wind and solar much more aggressively along with pumped hydro in a more recent development. It is likely China will burn a lot of coal and have what seems like an excess of coal plants but the power mix is still drifting to be cleaner over time. It is also unclear what can bring China back to its torrid pace of energy consumption: real estate is moribund and the exports goods boom has ended with global consumption swinging back to services post COVID. There is every chance this decarbonization accelerates on lower overall energy demand.

For transport over a quarter of passenger vehicle sales in China are now EVs and that no doubt will grow. The implications of this are as follows:

Chinese imports of energy are likely going into a more or less structural decline, especially if we look at imports excluding Russia and Mongolia. I’ve written about Mongolian rail and the like, but in the event the conflict ends China is already working on new pipeline capacity to Russia. “Friend shoring” is not just for the rest of the worlds viz China. This has distinctly bad security implications for any other countries on the East China or South China Sea - they would be well advised to make a similar rush for decarbonization and energy security if they do not want their strategic position to erode.

China’s domestic inflation is becoming increasingly disconnected from the vagaries of global fossil fuel markets, and their trade surplus will grow. This makes some of the anticipated losses from moving production out of China less of an issue and makes the country much less vulnerable to capital outflows.

China is again competitive in energy intensive exports at a time when there are shortages. Chinese exports of coke for steel making, steel and aluminium are up sharply the last few months and I would guess they are going to go a lot higher yet this year. An energy shock abroad affords China the demand to make its dismount from excessive real estate construction a lot more smooth. Construction can slow so long as upstream impacts are limited. So long as hot rolled steel costs 100% more in the US and Europe than it does in China, that is quite easy to manage.

Not every country is China, but Western Australia has done the right things. Its grid is already ~35% renewable, it has gas reservation so power prices are manageable and is planning an exit from coal using storage and particularly pumped hydro. The China playbook is not exclusively available to China.

That concludes my complaint. There are better options out there and they are not being taken, and it disappoints me. China gets plenty wrong but this material capacity building is something they get, and something that has real implications for inflation and consumer welfare. I wish it was taken more seriously among the Anglosphere political class. Perhaps this is the shock we needed for that change to happen.

Expect China's GDP growth this year to be $1.1 trillion, about the same as 2011-2014, more than sufficient to keep wages rising at a satisfactory pace, and a stark contrast to America's and Europe's expected contractions.

It's hard to maintain the Western narrative in the face of such stark differences in performance, especially in light of 2 million Western Covid deaths.