Weekly Wrap

Openai / Sam Altman

I have nothing to add here, but congrats to JP Morgan Research for this:

Hot New Unobtainium Just Dropped

With lithium, nickel, cobalt and other battery materials prices collapsing everyone is now concerned about phosphorus. The reason is clear enough: lithium iron phosphate batteries require it.

There is a good solution here aside from mining and it is 💩. As most high school chemists could tell you Adenosine Triphosphate is the energy currency of life and there is a lot of it in all plant matter and waste. Much of it is released in sewage and can be recovered via struvite (magnesium ammonium phosphate) deposition - a good piece by Veolia is here. The recovered material can be used as fertilizer which in turn frees up more material for batteries. If you really wanted to you could use the fertilizer to extract the Phosphorus and use it in batteries. Either way this attempt to fit up a widely available product that is mostly washed down the drain as the next unobtainium is deeply silly. We could instead pollute waterways less and have more material for batteries at the same time. Sounds good to me.

Thinking About How to Manage Entanglement with China

This is a great piece by Matt, worth reading in full. There is a certain model and set of patterns to China’s growth and there should be a similar set of counter patterns to manage the adverse side effects of that growth in particular China’s new green gluts summarized well in this WSJ piece.

Energy Modelling for Shocks in the Mid Transition

I took part in a talk Phenomenal World on oil and geopolitics in the Mid Transition - a term used for the period when fossil fuels are starting to flatline or fall but are far from out of the economy. I really enjoy these formats because sometimes things come to me or become clear that are less so when working very narrowly on a problem.

There is an enormous body of work modelling energy transitions and decarbonization for various economies, regions, sectors and the like and it is by and large very good and impressive. It is also, generally speaking:

Not graphical or sensitized to fuel transport, sourcing and logistics. A massive exception here is electrical grid modelling which is very well attuned to this but as grids are national or regional affairs the modelling stops at the grid’s edge.

Because of this, not sensitized to the kinds of geopolitical shocks that tend to create the largest energy shocks.

I think some of this is a legacy of the 1970s and how people thought about what an energy crisis was back then: running out of oil, overpopulation and the things that occupied the Club of Rome and animated the film Soylent Green.

The problem is that this frame of thinking - outright long term scarcity of goods - does not seem to fit what we have seen. Substitution effects are strong, alternative energy technologies are available and yet we still have shocks like the Ukraine invasion and could well have more depending on how toxic the Middle East gets.

Modelling in this space needs to consider not just networks of production - how much coking coal it takes to make steel, and how much steel is required for construction - but also networks of distribution of those basic commodities. The world did not run out of gas when Russia throttled flows to Europe but Europe had vastly less available gas and particular gas at a particular price. Similarly the shocks from sanctions on Australian coal did not destroy any output but did create logistical problems. For commodities that have low value density and complex global supply chains like oil, gas and coal these logistical details are very important and not managed well by canonical models like MARKEL-TIMES and other core models at places like the IEA. For an international energy agency to provide more useful and timely information a turn to these considerations is long overdue.

Chinese Power Demand in October

Strong, particularly in Southern China and particularly in those sectors that make up China’s new investment focus. Quoting www.sxcoal.com here, bold highlights mine:

Total electricity consumption in southern China's five provinces and regions, including Guangdong, Guangxi, Yunnan, Guizhou, and Hainan, reached 1,319.5 TWh from January to October, marking a 6.8% year-on-year increase, according to China Southern Power Grid Co., Ltd.

The high-end manufacturing sector continued to play a vital role, with electricity usage maintaining a high growth rate of 12.7% year on year. In automobile manufacturing, electrical machinery and equipment manufacturing, and other related industries, up 15.6% and 16.1%, respectively.

Notably, the electrical machinery and equipment manufacturing industry, as well as the computer, communication, and other electronic equipment manufacturing industries, experienced rapid growth, both exceeding 12% in growth rate. The power consumption of low-carbon transition-related photovoltaic equipment and component manufacturing even surged to 43.3%.

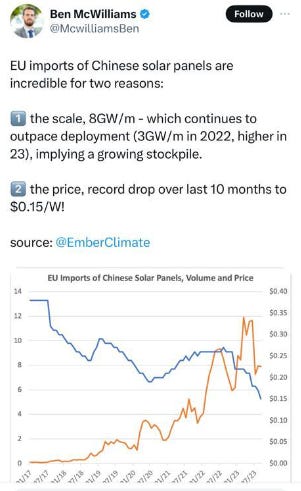

Two caveats here - due to COVID peaking around this time last year some of these year on year numbers will look stronger than normalized numbers will in six months but the growth in key export sectors like EVs, solar and the like are very strong. Whether this can be maintained will depend on whether China can continue to export or dump this output abroad, something many people are now noticing.

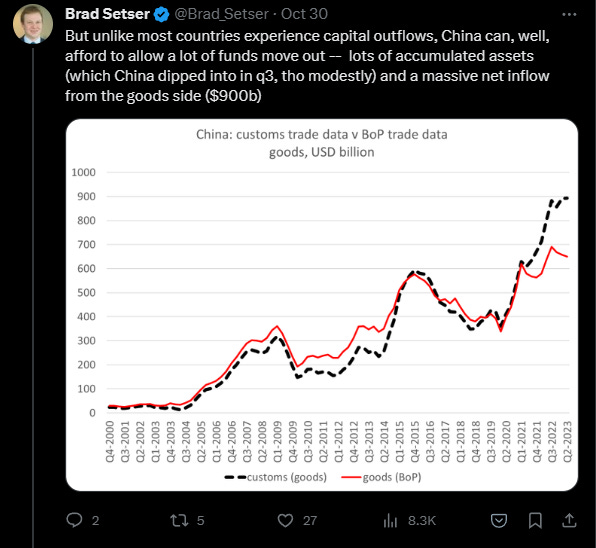

China now has an emerging problem in that these industries have grown so fast it is not clear that demand within China can keep up and exports are coming up against more and more trade friction. Similarly China’s reserve accumulation continues despite stronger outflow as noted by Brad Setser.

One option for China would be to turn all its Belt and Road Initiative lending and reserve accumulation into assets that provide financing for purchasing its surplus of solar, storage and EVs in emerging markets. There is a clear opportunity here for China to team up with local banks in say, Nigeria, and provide securitization lending to allow a much faster and more affordable roll out of solar plus storage. China gets more non treasury issued USD assets, China continues its green export spree, the Global South decarbonizes faster. What is not to like, assuming one is not an energy export dependent country in the Middle East? China can move from pushing its surplus onto developed market consumers whose governments are pushing back to pushing it on global fossil exporters who can do precisely nothing. I see no problem here.

> There is a clear opportunity here for China to team up with local banks in say, Nigeria, and provide securitization lending to allow a much faster and more affordable roll out of solar plus storage.

If China were to export to EM countries (that actually need FDI) and not to DM countries, that would indeed be an ideal solution -- trade frictions with the West would be reduced and poor countries would benefit from investments that actually improve their economic growth.

However I’m pessimistic. Michael Pettis has shown how China’s BRI investments have actually declined, and he attributes that to China learning the same lessons that previous trade surplus countries did -- such investments carry high risks.

For instance, “Chinese lending in Africa dropped to a new low of $994.5 million in 2022 from its 2016 peak of $28.5 billion.”

https://www.voanews.com/a/china-and-the-lessons-learned-from-a-decade-of-the-bri-/7301915.html

Ha well played JP Morgan