Eastern European Gas - The Baltics

The problem and some options

Following on from my previous post there are some acute issues with getting off Russian gas in Eastern Europe but also a range of policy options.

Firstly, logistics: there is not much landing capacity for LNG or capacity to run pipelines from Western Europe there from most of the gas modelling: no doubt ENTSOG is running some better models now. Per Gernot Wagner’s latest piece they had not done that in their latest modelling which is negligent from where I am sitting. They do make good maps which outline the problem:

All the sites circled in yellow are proposed FSRU installations that are not up and running as of yet. They include:

Gdansk: A big terminal capable of landing 6.1bcm/y, about a third of Poland’s gas demand. Sadly as of latest reports it won’t be open until 2028. Given it doesn’t take that long to build FSRUs and much less to convert gas carriers, I expect this timeline to tighten up.

Skulte: A terminal of 6.2bcm/y which can cover multiple years worth of Latvia’s imports. Not open until 2024 which is not that helpful but is close to a large storage site. Between this and Gdansk,

Paldiski: Seemingly less likely than the two above and only ~2bcm/y.

Tallinn: Similarly small at 3bcm/y per reports and also seemingly shelved.

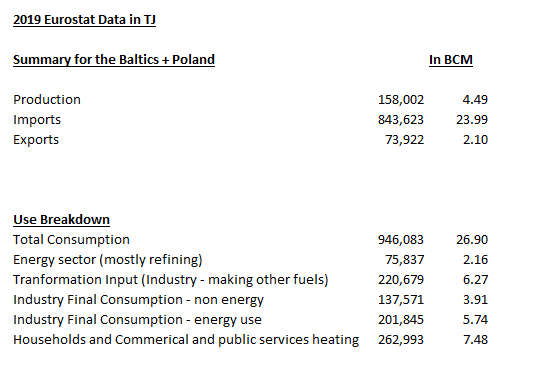

The Baltics + Poland group consumed ~25bcm in 2019, so with Klaipeda and Świnoujście that takes them to ~75-80% covered using LNG infrastructure if they can get Gdansk and Sulte done quickly. That is not a bad place to start from but will require a wartime level of focus and drive and not overthinking the possible impacts on Baltic sea snails or the like or anything else that might slow construction.

In terms of patterns of consumption they are all fairly similar. I have provided a snapshot of the IEA Sankey chart for Poland below but you can find them for the other Baltics here.

As you can see above the key sectoral consumers of gas are residential heating and industry. Poland uses relatively little gas for electrical power (~9%). So the name of the game here is generation of heat for homes and industry.

The breakdown for all three combined using Eurostat Data for 2019 is below:

Households and commercial buildings demand is big - so how much of that is addressable without outright demand destruction? Similarly how much of that industry demand can be reduced? Quite a lot according to the European heat Pump Association. While high temperature heat applications require temperatures upwards of 150C most food and consumer manufacturing does not. Outside of steel, cement and petrochemicals heat pumps are a clear option for European industry.

A more refined, model based analysis executed by Wolf and Bles1l comes to the conclusion, that the technical potential of heat pump use in industry across the 28 EU member states is 1717 PJ (477 TWh), with only 270 (75 TWh) or 15% of it being accessible if economic and practical considerations are applied.

What were those assumptions? Gas prices we are unlikely to see ever again and carbon prices around 20 euro. I think it is safe to say the TAM has grown since then.

So how well do heat pumps work? Happily there’s a literature on this and it is unequivocal: mid 20% area IRRs for consumer heat pumps and that was before power prices in Europe went up 5-6x. The question at this point is not whether this is a good idea but how quickly it can be rolled out. Savings in the order of 70% of energy but close to 90% for gas reduction are the norm. Gas reductions depend on the grid because you use no gas and instead use electricity. Bonus if you have solar onsite or your grid is not gas heavy).

A lot is going on so I will leave it there: but the question at this point is now how quickly Europe can install heat pumps and build LNG terminals before next winter.

Edit: A friend sent me this post on DIY heat pump installs and the savings, very timely.

Integration von Wärmepumpen in industrielle Produktionssysteme - Potenziale und Instrumente zur Potenzialerschließung