The People's Central Bank of Oil

A few thoughts on China's SPR

China’s Strategic Petroleum Reserve is a tricky thing to write about. Firstly, for onshore analysts the China SPR is a bit like fight club:

“The first rule of fight club is you do not talk about fight club. The second rule of fight club is you do not talk about fight club.”

Pricing authorities and alt data providers do not dare provide SPR estimates in China and investment banks are similarly reticent and I understand this is due to the fact that the SPR is considered to be very sensitive. It is also very hard to measure exactly: much like the United States’ SPR the oil is stored in underground caverns which do not lend themselves well to satellite imagery. There are excellent data providers who will give you a good idea as to the quantity of above ground storage. Those providers are not free, but then again trading oil with a structural data disadvantage is not either.

So, can we know anything about China’s SPR size? Quite a lot actually thanks to a little accounting.

China imports crude, exports very little crude and reports monthly refinery “runs” or how much crude goes into its refinery system to produce diesel, gasoline, petrochemicals and the like. So simply enough:

Imports - Exports - Refinery Runs + Oil Production = Change in Storage

This can then be accumulated monthly over time to get a picture of overall stocks of crude in China. Blue line is the back solve, orange line is a data provider disclosing what they can see.

That is… quite a lot. So much that if you look at global stockpiles of crude including this back solved number the overall picture of global stocks looks very different.

Which looks very different to data from some more bullish folks like Eric Nuttall.

The key here is “directly observable”. China’s SPR is not directly observable. In that respect China’s SPR is a bit like a black hole in astrophysics - you can’t see it, but you can see its impact on nearby matter through its gravitational force. Regrettably, when one of the world’s largest importers is so secretive you have to resort to indirect methods to find the data through mass balance accounting.

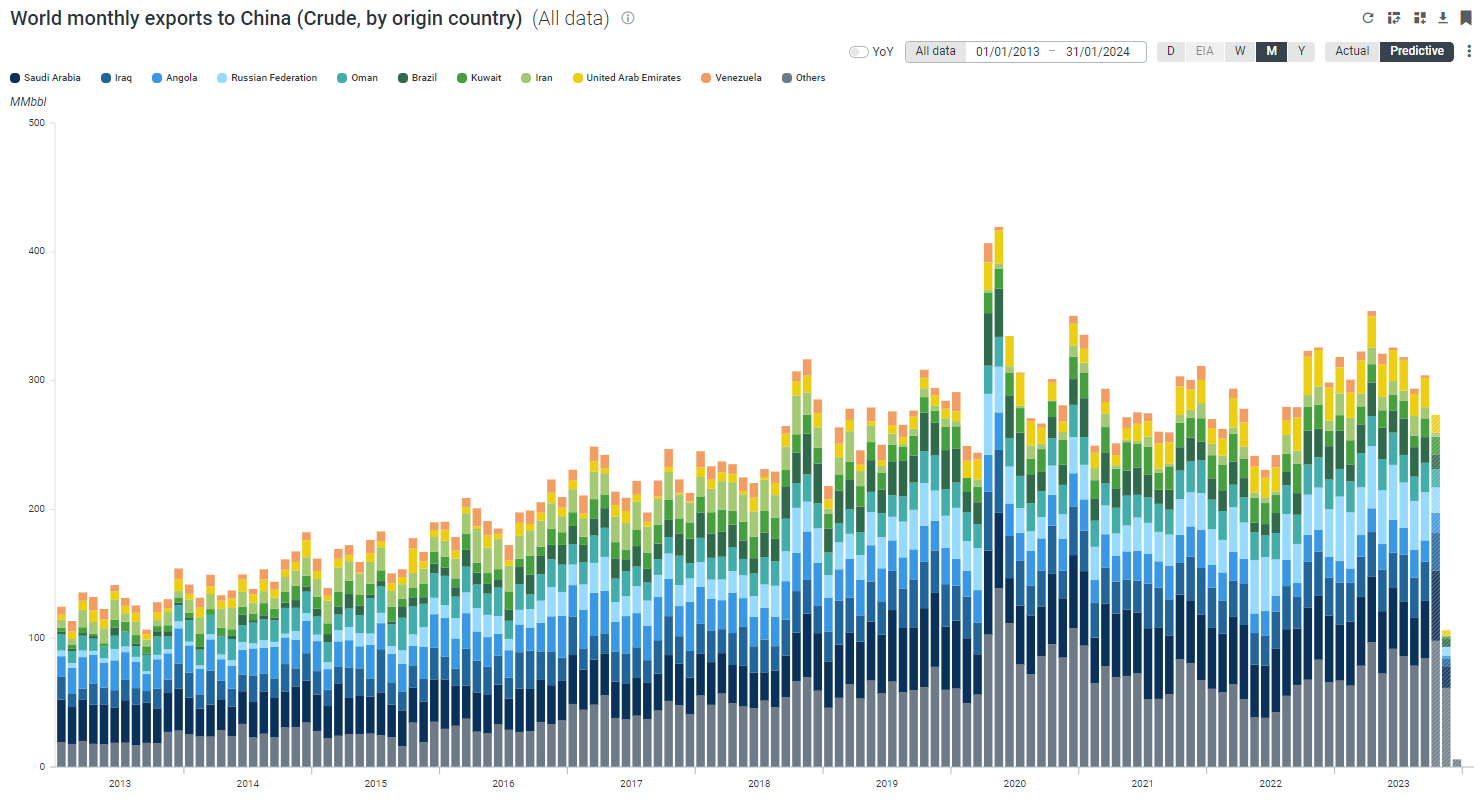

So, China’s SPR is very big - but what does this mean for oil markets? You can see how China uses its SPR through its quite wild swings in oil imports over time:

China clearly built this stockpile very aggressively in 2020 when prices were low, backed off imports when prices were high in early-mid 2022 (also when China was in some state of lockdown), opportunistically bought more in Q2 2023 and now seems to be backing off very quickly. China’s SPR seems to be broadly used to manage a range for oil and given its size it has a lot of capacity to do so.

The more interesting mystery in China crude and products is demand for oil products.

This is all calculated in a similar manner:

Apparent Demand = Refinery Runs + Imports - Exports

Aviation Kerosene looks totally normal. Covid lockdowns and reduced flights reduced demand in early 2020 and then again as China lost control of Covid in 2022. Gasoline had similar dynamics - nothing much to see there. Diesel, however, is just bizarre. China’s diesel demand was in secular decline pre Covid due to moving coal transport from trucks to rail and a move from diesel to gasoline for light delivery truck and bus fuel power trains along with a general trend to gasoline and electrification in passenger vehicles. To see diesel demand this strong with so much construction equipment idled or working less hours due to a real estate slowdown is strange. It especially does not line up with traffic measurements of trucking volume.

Alternate data providers estimate China has in the order of 200mm barrels of diesel and growing. So what is that for? The usual suspects have their views which are somewhat predictable and Taiwan blockade related and China has recently called for more secrecy on energy issues which is not entirely helpful to the case that this is not a big deal. What makes this especially odd is that China has not raised its export quotas for oil products for the fourth quarter. China normally dumps the inevitable surpluses that emerge from a production oriented model into the market: electric cars, solar panels, batteries, steel and normally diesel. China’s prodigious surplus from its Covid lockdowns and high refinery runs last year were what kept diesel prices from exploding upwards last year.

China is infamously opaque but in crude it has proved to be a moderating force via its SPR buying low and selling high to keep prices in a reasonable range but something else seems to be happening now with diesel. It is a little like Singapore’s Monetary Authority managing a currency band - interventions happen but only at the extremes of the range. Once again, you know them by the change in the order book not by public pronouncement or timely disclosure. Crude behaves like a managed currency but diesel appears to be experiencing some kind of structural break.

If you have any good ideas why a country would want to have in the order of 60 days of inventory in an oil product that has a finite shelf life, let me know in the comments. One takeaway for me from a markets point of view is that China either needs to sell a lot more diesel abroad, cut imports sizably or some secret not very good third thing.

Thanks, this is a great piece.

Did you put CTL into this? EIA has China doing 124kbpd of CTL in 2021 (possibly higher now), and I think most of that is going into diesel/naphtha. I realise that might be even more diesel to account for...

I have felt this way with regard to iron ore. Property sales down 40-60%. FAI private sector proportionately weak. Yet steel production up. Commentators say "well, it is EV's, and solar / wind capacity installation, that's why steel demand remains strong". But then why is copper, lithium, scrap all so weak. Your oil analysis above seems to match well.