Xinjiang and Polysilicon

How crucial is Xinjiang in solar supply chains?

There has been no small amount of discussion of Xinjiang and solar supply chains. Here I am going to take a step back from the hot take merchants and evaluate this from first principles in this piece, and will follow up with a second one on what policy measures would be sensible assuming there is anything undesirable here.

Looking at this problem from a basic business optimization point of view the name of the game is getting everyone the solar panels they demand at the lowest cost. In operations research this is called a minimum cost flow problem. We need panels to be made, they need to be distributed globally to customers and there is some mix of fixed and variable costs in locations and transport costs. If fixed and variable costs are pretty much the same everywhere and the goods have high transport costs or are perishable then you make products close to customers. That is why your pizza comes from close by. If fixed and variable costs are wildly different - chips in Taiwan and iron from Australia instead of vice versa - then geographic specialization tends to occur.

So before jumping in with hot takes its worth asking:

Does Xinjiang have some kind of transport cost advantage in being close to customers? It is not close to customers so this can readily be ruled out.

Are there softer reasons here that do not fit in a more quantitative analysis, alternately, is this the wrong model? This might sound silly for a chemical product but for fashion goods and even cars where something is made is part of the customer’s subjective experience. Additionally is there some know how that is not replaceable? Has the US or Europe lost the ability to do this? I find this less plausible since the US and EU and Japan all make polysilicon - they’ve just been losing market share in solar polysilicon which is slightly less pure and lower specification while retaining their position in electronics grade which is higher specification. So, this is not worth spending much time on - this is a close to commodity product.

Does Xinjiang have some advantage in variable and fixed costs in polysilicon? Is there some kind of technological edge that explains how it went from nothing to this much market share so quickly? What goes into polysilicon and what drives Xinjiang’s competitive advantage assuming there is one? This seems to be what has driven the changes in this market and is the focus of this piece.

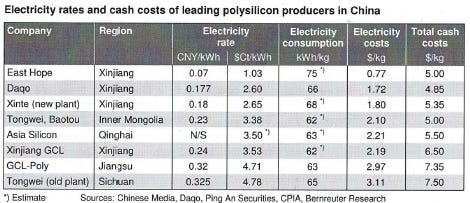

Wacker has a good guide to what goes into making solar silicon here. Without getting too far into the weeds the key inputs are quartz and energy - capital equipment and consumables are much the same the world over. Other notable costs common to any industrial site - grid connection, land, roads and basic construction are not and heavily driven by local labor costs and land scarcity. In Bernreuter’s most recent report they outline recent capital expenditures for Chinese plants and what drove the rush to Xinjiang:

It goes on with electricity costs. With a share of about 30%, they make up the largest component of cash production costs. Most new Chinese polysilicon projects have been built in Xinjiang and Inner Mongolia because coal-fired power plants in these two regions offer very low electricity rates. An extreme case is Xinjiang East Hope; its captive power plant uses coal that is transported by a conveyor belt directly from an adjacent coal mine, resulting in an ultra-low electricity rate of only CNY0.07/kwh.

How much energy per kg? As per the below a ton of polysilicon uses 60-70MWh per ton, roughly seven times the energy intensity of aluminum. It is congealed electricity though the efficiency has improved a great deal over the last decade.

Why unit capital expenditures for plants are so low in China is less clear though substantial land availability and strong subsidies and incentives to locate plants in Xinjiang no doubt play a role. Unit labor costs according to NREL are so low - less than 500 FTEs per 20,000 metric ton per annum output plant - that wage costs are not a key driver here especially after a high degree of wage differential compression between China and the EU and US.

So, we have our answers as to why all the polysilicon production moved to Xinjiang: muscular industrial policy and cheap electricity. If Xinjiang ran on renewable energy and there were no labor abuse allegations then perhaps that would be the end of the discussion: China has a comparative advantage. The problem though is that Xinjiang runs on cheap coal which may or may not be mined by people working against their will. I find the discourse on labor issues in Xinjiang so unhinged I won’t go down that particular epistemic rabbithole and instead focus on emissions.

I’ve suffered through some truly painful interactions with bitcoin promoters saying Xinjiang’s power grid is low emissions and let me just leave the chart below.

All data comes from China’s Bureau of Statistics and comes via CEIC. Xinjiang and Inner Mongolia run on coal and there is a very good reason for that: the coal is cheap at around $20-23 per tonne due to geology but also “remarkably low labor costs” - whatever that means - according to some very tactful consultants. Often the coal mining and polysilicon production are closely linked. You can see this with the East Hope production complex Northeast of Urumqi where the massive coal pits are located close to the power plant and polysilicon plants.

At those coal costs, and roughly 300kg of coal per MWh of power you can readily get to around $10 per MWh power costs, and with that approximately 70c of power cost per kilogram of polysilicon. In less tightly integrated locations costs are still low but, once again, its entirely coal driven. This is how China gets to sub $10 per kg of polysilicon.

What is important to note here is that power use per kg of polysilicon is lower because these are new plants that use less power per kg. China can continue to push the frontier of efficiency and crush pricing. That leads to underspending on capital expenditures and improvements at US plants which leads to a hysteresis where US plants fall further and further behind on unit efficiencies while also losing customers in Taiwan as China runs competitors out of business using soft credit constraints. If this sounds like some of Employ America’s work on what went wrong in semiconductors and a path dependent process that is exactly what it is.

China’s advantage has been a combination of no emissions constraints, muscular industrial policy and a seeming indifference to short term financial viability or oversupply issues in these markets. Emissions intensity per kg of polysilicon is now high and going to get worse as these provinces take further share in production. Even if there is cheap power elsewhere a lot of capital has been scared away from this space because of Chinese producers disregard for capital returns and their bankers willingness to fund high leverage and losses to consolidate the sector. As a result the US and Europe consume about 60GW of panels per year, at ~3g of polysilicon per Watt that is 180,000 tonnes of polysilicon and the US and Europe produce about 110,000 tonnes. Not an insurmountable gap at ~$3bn of capital expenditure1 to move to self sufficiency in polysilicon and no doubt avoid a large amount of emissions and labor rights issues. However this is something the US and Europe will need to provide clear signalling on: if China can dump into the US, and the US downstream solar sector dies again then we are back to the beginning.

That is enough for today, I’ll discuss potential trade approaches and actions - and their unedifying history of haphazard implementation under the Obama administration for the next piece.

70,000 tonnes multipled but $40 per kg unit capital expenditures which is an old and high estimate.

Hi Alex, The numbers out of China need to be treated with caution. It is important to differentiate silicon production and polysilicon manufacturing. A polysilicon plant has a short lifetime, and most CN producers quote cash costs of production, whilst ignoring plant depreciation. On a $/watt comparison, cell /panel prices are coming back up from the heady days of cheap at all cost. Quality is now a factor, which goes all the way upstream to raw materials. There is a strong opportunity developing in the US and Aus for domestic production.

This is an exceptionally well written piece, and deftly opens up some rather unique issues inside China's industrial landscape. I'd like to see alot more of it.