Should the USA or Australia Make Solar Panels?

Getting down to relative costs and risks in detail

There are a lot of extremely high conviction opinions on this particular issue with strikingly little analysis backing those views. I got into an argument online about this recently and thought it would be good to rigorously step through how I think about this and how my thinking has changed over time.

There are two reasons you might want to make something in your country versus importing it.

Reason 1: Competitive Pricing

You can compete with other producers on pricing. This pricing is not just “factory gate” pricing, but the price delivered to your consumers and adjusted for any major externalities – like carbon. This is a subtle point but for bulky low value goods the logistics is really important, for something more high value per unit of weight or volume it matters less. I discussed this in a previous piece here with regards to what markets were likely to be disrupted by the Ukraine conflict and my analysis was correct: the markets where logistics mattered more were the most heavily impacted.

Transport Costs

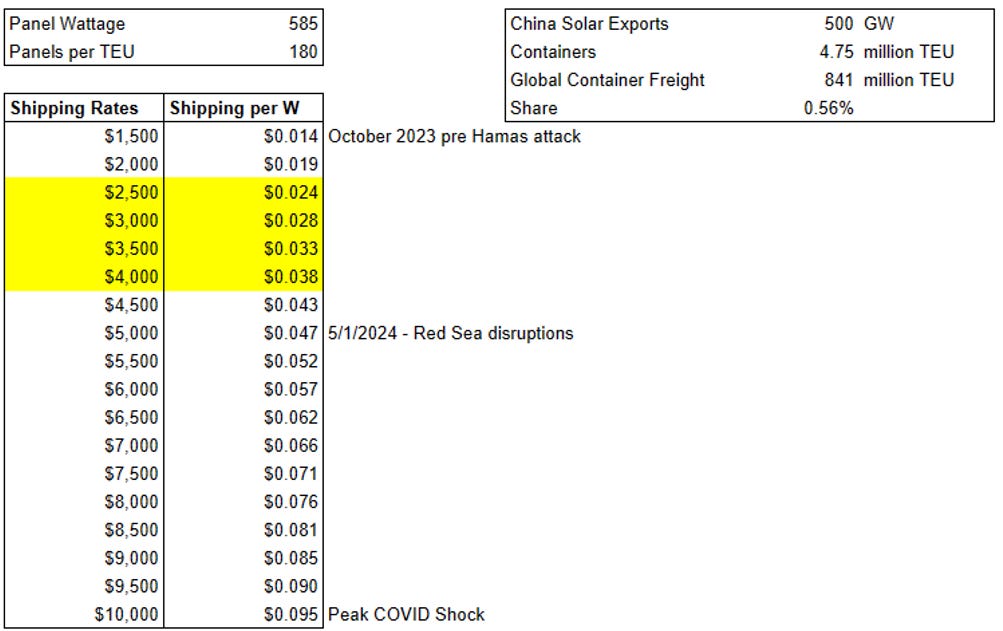

So for solar, what are transport costs? The Freightos Indices measure the price of a TEU – twenty foot equivalent unit – shipped from Shanghai to the West Coast, and Shanghai to Rotterdam which are the dominant container shipping routes and particularly so for solar. Recent volatility in shipping has made the question of what is “normal” here far from clear. It would be reasonable to expect that unless geopolitical risk falls that shipping rates might be much higher going forward.

So how many panels and watts go in a twenty foot container? Longi’s Hi-Mo-7 (not a strategy for outperforming the S&P500) has a specification sheet that indicates that you can put 180 modules in each container. At ~600W per panel you get a table like this for per Watt shipping costs:

By this calculation 2.5-4.0c per Watt is the premium you should be willing to pay for onshoring on transport alone – because you are going to pay that anyway in shipping costs though perhaps that is not high enough based on recent headlines.

Disruptions like these have real costs as outlined in a report from ARENA:

Carbon Costs

Unless you are part of that miniscule intersection of the Venn diagram that believes both solar is good and that carbon border adjustment taxes are bad – that is, you login from Beijing and work in a PR and communications capacity for the government – carbon costs are real.

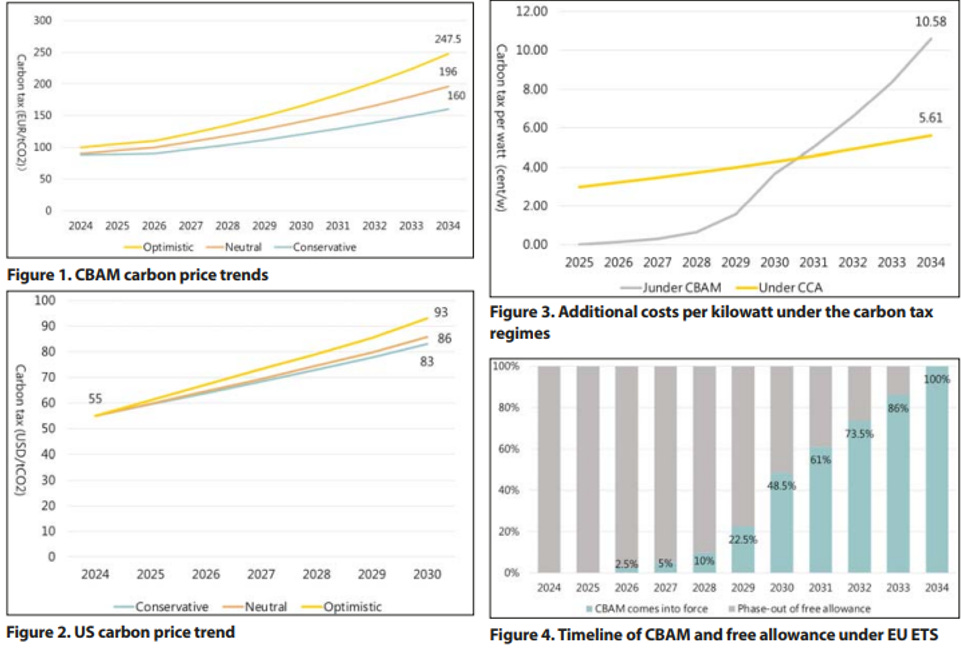

Carbon in solar panels normally comes from upstream production of polysilicon and wafers. I outlined some of these cost and emission differences in a previous piece here. In a recent PVTech Insights Piece “The Costs to the Solar Industry of a Price on Carbon” which outlines some of the scenarios for cost impacts on panels for different carbon prices.

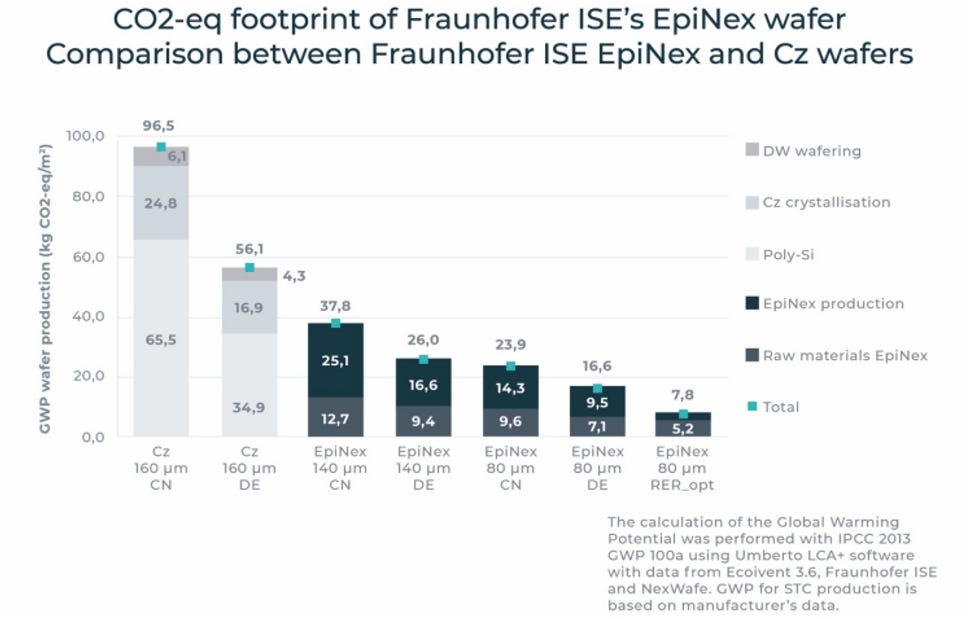

This all depends on how high the emissions of making panels are as shown below.

And that largely comes down to the aluminium framing that makes up around 9% of emissions, and polysilicon and wafer that makes up 50% or more. There are solutions on the framing side that use recycled steel and there are new direct deposition wafer processes from the likes of Nexwafe (full disclosure, am an investor). To that end you can see for 2028-2030 that leading edge HJT cells with thin direct deposition wafers and aluminium free framing saving in the order of 350g of carbon per Watt. At $100 carbon that is another 3.5c/W of premium that should be attached to leading edge production outside China.

In total a 7c/W premium for onshoring production is a reasonable baseline for carbon and transport savings. This excludes the carbon of the transport itself among and other potential carbon reduction approaches.

What About Actual Production Costs?

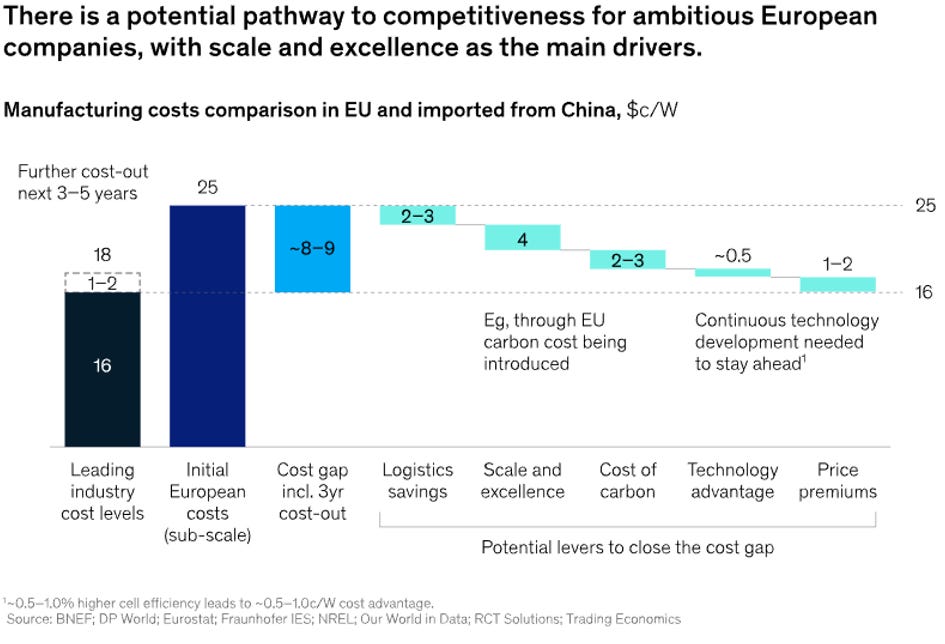

There have been several studies long these lines. One is from McKinsey in 2020 called “Building a Competitive Solar-PV supply chain in Europe”. The numbers are a few years old but still largely accurate – they come out with a higher reshoring premium than me but not by much.

The Australian Photovoltaics Institute (APVI) produced longer but oddly less detailed report here. It provides a breakdown of relative competitiveness and comes out strongly in favour of onshoring module production due to relative competitiveness using imported modules.

Upstream looks significantly less favourable but assumes no technological improvements which is odd for a government agency that is meant to stay on top of these things.

Similarly, cell manufacturing looks tough mostly due to silver pastes – which is also a weird thing to say when one of the domestic companies has the best copper metallization technologies today which would make that irrelevant.

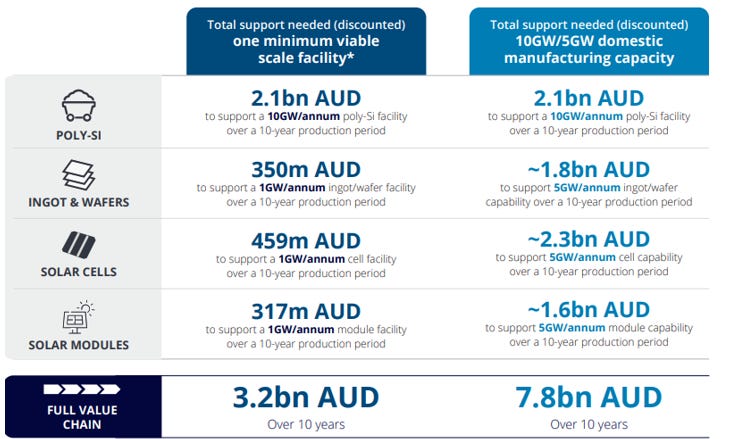

As you can probably tell by this point, I do not hold this report in particularly high regard. The message seems to be “we suck, we can’t be better, here are the subsidies required to close the gap”. The numbers below from the deck are enormous and a highway to Peronismo. And perhaps that was the point all along, to get the highest subsidies possible by sandbagging costs.

For polysilicon to wafers, you could use the Epiwafer process. Forecasts there are 5c/W capex at the 15GW level for every step from MG-Si to wafer or 6c/W at the 7GW level. Lets call it 5.5c/W at 10GW – that’s US$550mm, add in some overruns as is the custom in Australia and that should work out to A$1bn. Not much support would be required because at these costs of ~3-4c/W for wafers you could just write a put on the wafers which probably would not be exercised. A put plus a government loan would a good way to do this. This would also net wafers around 4c per Watt on a sustainable basis. Metallurgical silicon to make precursor silane gases is produced from a reducing source (coking coal, mostly which Australia has no shortage of) and electricity. It could be imported from China as noted in the report - but China has a 55% export tariff for export to Australia. The report then notes that:

In particular, Australia's solid and longstanding relationship with China in the solar sector could be a defining factor in the success of Australian manufacturing.

This is yet another example of how China is very shrewdly throwing sand in the gears of efforts to decouple or develop solar elsewhere and how some Australian government departments seem to be completely delusional as to how China is likely to approach this. If they are already imposing export taxes on key inputs are they really here to help you? Probably not.

For downstream I think the estimates in the APVI / ARENA work are far too high and I question the estimates because there is no detailed breakdown of the tool chain and process chain to understand where the constraints like. Happily, there is vastly better work being done elsewhere.

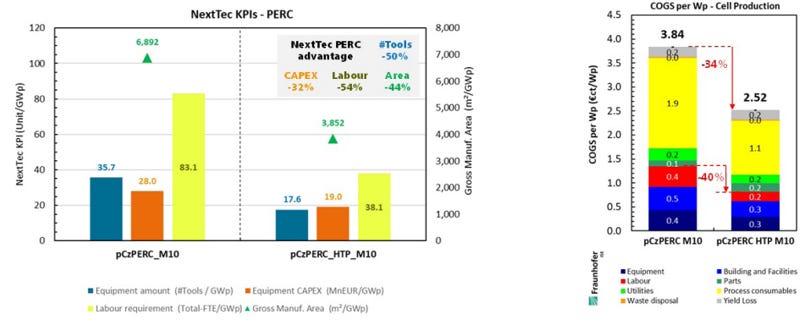

In PV International’s 50th edition there is an article called “Next-generation high-throughput cell production technologies – impact on equipment CAPEX, footprint and labour requirements for a 10GWp PV cell factory” by B. S. Goraya, F. Clement, S. Nold, at the Fraunhofer Institute for Solar Energy (ISE). While I understand even my readers might be reaching their limit for getting into deeper cuts of industrial optimization exotica this is far better work than the APVI paper because it goes into the detail of how better tooling that operates at faster rate can reduce costs. The punchline is below:

The results show that an increase in throughput leads to a reduction in each KPI and the TCO for the PERC-HTP route when compared to the reference PERC processing route, with the relative advantages being:

• 50% reduction in the number of tools on the production line (in tools/GWp)

• 32% reduction in overall equipment CAPEX (in €m/GWp)

• 44% reduction in gross manufacturing area (in m2 /GWp)

• 54% reduction in labour requirement (shift-FTE/GWp)

• 34% reduction in TCO (in eurocents/Wp).

And here:

So not only do these calculations show that the estimates for current technology are half what the ARENA report indicated, but that leading edge approaches with high throughput come out closer to 2.5c/W.

All in costs – assuming you use leading edge approaches through the full stack get you to 4c/W for wafers, and 2.5c/W for making cells. What do cells cost today in a market where everyone in China is losing money and often making negative gross margins? 6.3c/W, according to spot prices on Shanghai Metal Market.

Using the NREL cost model to estimate the cost of turning cells into modules as per below:

I get the numbers better than indicated in their “economies of scale” case:

Wafer: 4c/W

Wafer to cell: 2.5c/W

Cell to Module: 6c/W

For an all-in price of 12.5c/W.

Even when Chines solar companies are running egregious losses due to overproduction the US or Europe or Australia can compete if they take a full-stack leading-edge technology approach. Add in the transport and carbon premia of 7c/W and they are far ahead without subsidies, though for the carbon this requires somehow internalizing the carbon costs of Chinese output via a carbon border adjustment mechanism which the US once again is far ahead on.

Reason 2: Supply Security

There is none. The McKinsey report has a chart that makes this abundantly clear:

China owns this market at this time and while China cutting off supply to the world deliberately seems unlikely when they are this oversupplied selective punishment is something China has done before. Whether it is trade actions against Lithuania or Australia it is abundantly clear that you do not have to be the United States to feel the wrath of China. A good leading indicator is how many angry calls various levels of government get from the Chinese consulate or embassy. Even in Australia where the temperature has dropped in the relationship, the glass jaws and switchboards at the Chinese consulate continue to be active. An obvious risk here is that in a maritime conflict in the South and / or East China sea shipping would be completely disrupted and there would be no panel exports. That seems like something worth hedging against, especially if it can be done at low or reasonable cost.

How Should Policy Makers Change This?

The Biden administrations trade actions have done plenty on this point but it is worth nothing that even with tariffs of 50% on panels if China is dumping at 11-12c/W with costs at 16-18c/W they might continue dumping because their costs after tariffs of around 16-18c are lower than US costs which haven’t full squeezed out direct deposition wafer efficiencies. This is all presumes the Chinese banking system will continue lending into losses which they might well do though overnight pronouncements make that less likely.

A better solution is what worked for the renewable sector: a combination of lending like that of the Loan Programs Office combined with contracts for difference or puts on production. Polysilicon and wafers are commodity products – so much so they have transparent pricing indices as you can see here from Shanghai Metal Market.

Part of the current slowdown in investment is due to existential angst around the election. Trump has flip-flopped before on Tiktok and numerous other issues and it is wholly unclear what he might do with the IRA and solar tariffs. Some risk aversion on the part of investors until some clarity emerges on that or until the outcome of the election is clear is understandable – hence some wafering capex cancellations by the likes of CubicPV. The way to get around this is to just work out what the quantity of domestic production is desired for poly and wafers and offer contracts for difference or puts on that output that cannot be rescinded by a new administration. These offers would generally be shorter than for utilities and unlikely to pay out unless the US went to zero tariffs and zero subsidies. This is especially appropriate for Australia which has had a great deal of success with CFDs for renewables and which seems deeply reluctant to get in another trade war. These auctions would also be technology neutral – the point is to get a particular wafer at a specified level of performance or better which encourages a race to the top technologically rather than a Peronist industrial hand out policy and “game of mates” dynamics.

My concern with the current settings in Australia is that efforts are moving more towards exclusive dealing with parties that have wildly uncompetitive projects. Quinbrook’s plans to build a standard technology polysilicon fab in Australia cannot pencil out by my maths – and I have restructured four separate polysilicon businesses. The risk here is that the politics swings from Mazzucato-inspired project finance boondoggles that make no sense to hard libertarianism and unconstrained dumping by China. Germany has recently chosen hard libertarianism on this point and its solar sector has completely collapsed since with job losses and even the equipment being shipped to the US in the case of Meyer Burger. Both of those options carry costs, fiscal and otherwise and the wastage of switching back and forth is enormous though will be a goldmine for consultants. Maybe it is wholly unrealistic to think Australia could do this properly and not just line the pockets of structurally uncompetitive interest groups and the consultancy complex – but I think it is worth a try.

How My Views Have Changed Over Time

I think about this very simply in operations research and economic terms. I am not a vibes-oriented analyst or enthusiastic about anything people describe as nation building. Making the call on any initiative based on the PR spin seems deeply unwise. Whether due to the travails of the political cycle or long-term efficiency arguments there must be a path to competitiveness over time once externalities have been internalized by carbon taxes or the like. Otherwise, the programs get cancelled at the next election or the cost is not worth the trouble. But as Javier Millei points out:

We do need to price and be explicit about externalities and fully loaded costs.

In 2015 the price of a solar panel was about $1.12/W. China’s costs were by most accounts 20-25% lower at the time and this was due to much less automation than we see today and lower wages in China - both of these gaps have closed very quickly since. Entering the market was harder because capex per Watt of any part of the chain was much higher. Shipping costs were also materially lower because drone strikes were something only the United States could do, and the Red Sea was much safer. US-China relations were much less contentious, and China had not at that point engaged in a series of punitive trade actions for political reasons. Paying a 25c per Watt premium for onshoring when the risks seemed a lot lower was a tall ask and the US and Europe took the reasonable view at the time that it was poor risk reward. We are now in world where unit capex is much lower, the cost spread is negative, and risks are vastly higher. I close with the world of John Maynard Keynes:

When the facts change, I change my mind. What do you do, sir?

Where does it say that China has a 55% export tariff for export of Silane Gas to Australia?

The China-Australia Free Trade Agreement (ChAFTA) schedule shows 0% for

Silicones in primary forms (HS Code 3910.0000):

https://www.dfat.gov.au/sites/default/files/chafta-explanatory-schedule-of-chinese-tariff-commitments-non-official.pdf