Weekly Wrap

In an effort to post a little more consistently I will be providing some links and issues of interest that have not yet quite got to very long and quantitative ones.

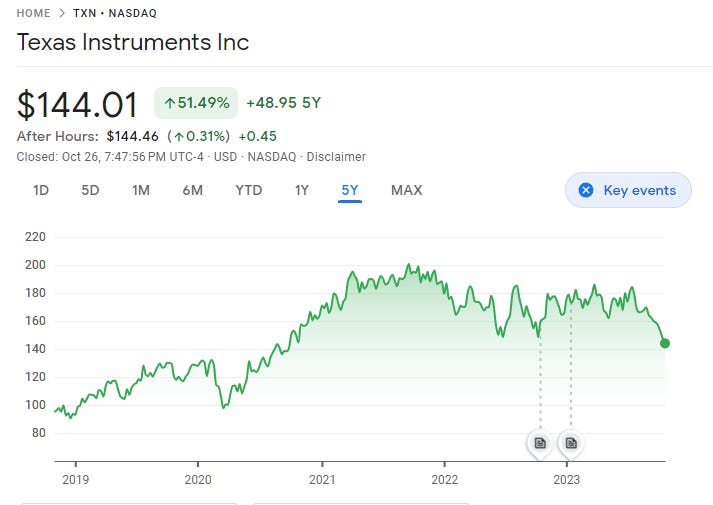

CHIP Wars Move to Analog and “Foundational Chips”

Silverado has a report covered here in bloomberg outlining how China is now dumping into sectors of the semis market that historically has sticky customer bases with high switching costs and good margins. Texas Instruments has long been seen as a “quality” name in semiconductors with much lower volatility than commodity memory players like Micron, Samsung or Hynix. That seems to be breaking down now, and violently. Onshore China producers of these chips have already gone into full price war mode and can be seen in the relative performance of Silergy.

The China overproduction hammer now seems to be coming for some previously safe names in US semis.

China’s Capex Shift and Its Consequences

China’s deliberate deflation of its property bubble and pumping up of its output of green technology has had some clear first order effects: weaker metals prices and much cheaper solar panels and batteries of late as well as a squeeze in inputs to the green tech boom like lithium though this deflating. What is more less well appreciated is how China producing a surplus of batteries and power semiconductors is now leading to dumping of solar plus storage, everywhere because the upstream surplus creates greater competitiveness downstream. Sungrow and Growatt are discounting heavily in Australia for inverters and panel prices are back to $0.15/W. This is leading to some fairly crazy discounting - 6.6kW and inverters for ~A$3,000, throw in a Huawei battery for another ~A$7,000 and my modelling of the annualized free cash flow yield from reducing a power bill is in the low teens. Australia’s distributed solar boom is only just getting started on this math, even with interest rates where they are. The two largest non-Chinese residential inverter producers seem to be finally “getting it”:

This is likely to continue crushing gas burns globally and, barring a generalized Middle East conflict, the price of fossil fuels will go down as this picks up. What is particularly interesting is how European solar manufacturers that produce Uyghur Forced Labor Act compliant panels are now selling into the United States which is rapidly eroding the cost of US trade actions on Chinese panels. So long as Europe remains open to Chinese imports the surplus in China is dumped in Europe and then Europe sells into the US. The spice must flow, after all. The question of course is - at what point does this become an economic security issue? China has a well-established track record of cutting off supply when it is displeased with trading counterparties so what sort of share of Chinese imports are acceptable and how should that be enforced?

This is likely to continue because China is producing so much solar its grid currently cannot take all its output - a good post from David Fishman here outlining how Guangdong is now grid constrained for more distributed solar. David may not share my politics but he is a first-rate analyst - pity he insists on staying on twitter, aka the bad place.

The Diesel Shortages Might not Last Long

One persistent and enduring problem from the Ukraine conflict has been elevated diesel prices and crack spreads. Russia produces heavier crude that has generally flowed away from Europe due to sanctions but, as I outlined in a previous piece, China does not seem to be buying that crude then selling the diesel. This problem might not last long however - diesel vehicle sales in Europe are in free fall and the auto mix shift is happening quickly. Whatever China does with its lake of diesel it might not matter that much as this process continues.

Norway is the bellweather here and diesel is having a particularly precipitous decline there:

Swiss data is very good (well, except for vote counting of late) and has helpful data on the stock of passenger vehicles by year. The diesel share of passenger vehicles fell from 29.6% to 26.75% from 2020 to December 2022. At this clip apparent diesel consumption in Europe is likely to weaken enough to make the Ukraine war matter a lot less, and soon.

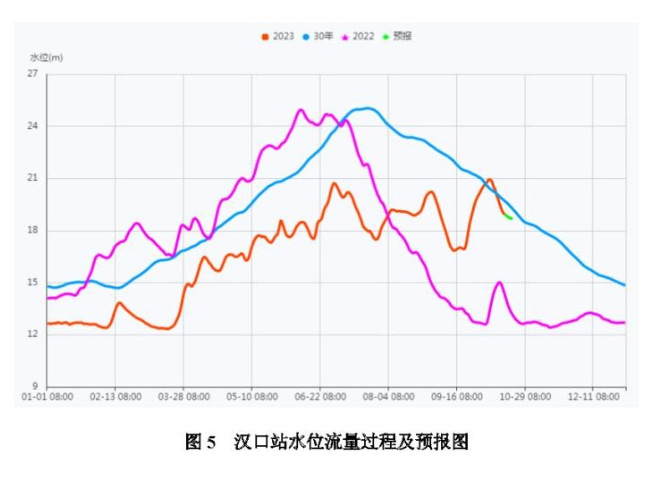

China Hydro - Its Back and It Matters (a lot)

China’s hydro drought appears to be breaking. Latest data from the Yangzi River Basin Authority show a sizable improvement in rainfall and river flow along with dam levels. Three Gorges Dam in particular seems to be back to being full:

Hankou, a monitoring station gives some sense of just how bad things got the last two years. Thirty year normal dam levels are in blue, 2023 in orange and 2022 in pink. 2022 was an unmitigated disaster with very high power demand and low rainfall leading to much lower reserves which did not really recover until the last few weeks. This all now seems to be turning around.

Perhaps more importantly the ECMWF forecasts are for a wetter Q1. All caveats that apply to weather forecasts apply here but it seems that 2024 is shaping up as a more normal hydro output environment.

China hydro utilization hours could rise ~20% which combined with more capacity would imply much lower coal burns especially as renewables take more share. IEA forecasts of China power emissions peaking this year look plausible.

This is fairly amusing as China seems to have panic imported a lot of coal the last few months just as the weather turned leaving them with significant inventories they will not be able to work down that quickly.

We have all been stopped out by risk management at the bottom or top at some point, but it is seldom you see it happen to the world’s largest power grid.

This is acutely important for Chinas’ coal imports because:

Most hydropower connects to China Southern Grid.

China’s south is where most coal imports go.

Big hydro years tend to be bad for thermal coal - while we will not know for sure until seasonal rainfall picks up next spring this is shaping up to be one of those years.

Wait - this sounds very deflationary!

It is. In mid 2021 people who focus more on commodities and upstream inflation drivers were generally of the view that central banks were wildly offside of inflation developments:

Services wages exploding in the United States

This tape seems to be running backwards right now and rates are very materially higher. Infer what you will.

Good thoughts on hydro... wish I could read mandarin or translate those reports!

Great writing, Alex. Do you have any thoughts on how iron ore has managed to stay so elevated, given the property deflating and weaker base metal prices?